Market-Making Models in Web3: Retainer, Loan/Call, Liquidation

Market making is a specialized service that can add significant liquidity value to a token issuers' businesses. Today we talk about accounting for the two common models of market making contracts.

Acknowledgments

I want to extend my sincere thanks to Isaac, Casper, and Jalal for their valuable contributions. Their expertise and guidance greatly enriched this piece, and I’m grateful for their support throughout the process.

Introduction

Market-making activities are subject to numerous legal controversies and should be carefully assessed to ensure that the exact service provided to the reporting entity complies with the laws of the relevant jurisdictions. A few legal cases against vendors providing market-making services in the US are listed below1:

Before diving into the detailed models, it is helpful to first clarify the core function of market makers (the “MMs”) in Web3. This context will provide a foundation for understanding the models discussed in the following section.

Market makers offer sophisticated services designed to ensure sufficient liquidity on both the buy and sell sides of markets where issuers’ tokens are actively traded. Consequently, market-making services reduce the bid-ask spread, facilitating easier and more efficient trading for investors with minimal price slippage.

To further understand these functions, it is important to examine the main market-making models. The next section draws on a post from Flowdesk, which identified two primary models (retainer model and loan/call option model). Additionally, we note an extra arrangement often used, which we refer to as the liquidation model.

1. Market Making Models

1.1. Retainer Model

Under this model, the company pays a monthly retainer and provides liquidity to a market maker using a mix of its own tokens and cash or stablecoins, which are returned at the contract end. Market makers often deduct retainer fees directly from loaned assets. As a result, calculating outstanding balances requires strict reconciliation procedures to ensure that each month's retainer is accurately recognized as an expense, even if it is offset against loaned assets instead of paid in cash. If offset, record a debit to the expense (or prepaid expense) account and a credit to the token loan receivable.

1.2. Loan/Call Model

In this model, the issuer loans tokens to the market maker, who provides liquidity and executes trades. Simultaneously, the issuer grants the market maker a call option to purchase tokens at a predetermined price. The market maker may settle the loan by:

Returning the original number of tokens or

Exercising an option (if the market price of the token exceeds the agreed-upon price) and returning to the issuer cash or stablecoins in the amount equal to the fair value of the tokens as of the inception date.

Under this model, the market maker is compensated via the call option and gamma trading of the option [Flowdesk].

The market maker uses the issuer's tokens to support buy orders, deploying them on the buy side of the market. The market maker provides cash from their own assets for these trades.

1.3. Liquidation Model (separate arrangements)

In addition to the above, market makers assist token issuers with the liquidation of tokens on the open market in a manner that minimizes the impact of such liquidations on the market price. This is an additional service that requires a separate accounting. In such an arrangement, a market maker acts as an agent of the token issuer. This is because TI directs how MM is supposed to use (dispose of) the asset, leaving MM to determine the exact timing and structure of the dispositions.

2. Accounting Process

This section reviews the accounting considerations relevant to typical activities that token issuers (TIs) undertake when engaging market makers (MMs):

Liquidity Provisioning

TIs transfer liquidity to MMs.

Operations

MMs use this liquidity to execute trading operations on exchanges. TIs monitor the receivable balance due from MMs. TIs also account for activities that affect this balance with MMs.

Liquidity Deprovisioning

MMs return the liquidity to TIs at the end of the contract term.

2.1. Liquidity Provisioning

“If an entity transfers a nonfinancial asset in accordance with paragraph 350-10-40-1, and the contract does not meet all of the criteria in paragraph 606-10-25-1, the entity shall not derecognize the nonfinancial asset and shall follow the guidance in paragraphs 606-10-25-6 through 25-8 to determine if and when the contract subsequently meets all of the criteria in paragraph 606-10-25-1. Until all of the criteria in paragraph 606-10-25-1 are met, the entity shall continue to do all of the following:

1.Report the nonfinancial asset in its financial statements…

…3.Apply the impairment guidance in Section 350-30-35.”

[FASB ASC 350-10-40-3]

After transferring tokens to market makers, subject to contract specifics:

TI may retain the ability to direct or supervise MM activities2.

TI may be able to direct MM to liquidate a portion of the tokens to finance operations and remit the proceeds from the liquidation to TI.

TI may be able to access information about token balances held by MM and market indicators from exchanges where MM operates.

Market makers must generally have the authority to direct the use of tokens in order to operate effectively and meet their obligation to act in the best interest of the token issuer. The extent of this authority depends on the specific contractual terms. Generally:

Under the retainer and loan/call option model, the TI (issuer) transfers control of the tokens to the MM (market maker). Derecognition means that the TI removes the tokens from its balance sheet and recognizes a token loan receivable at its fair value at the time of transfer. See the respective section below for details of accounting for token loan receivables.

Under the liquidation model, TI retains control, and the tokens remain on its balance sheet. As a result, market makers’ trading operations will result in the recognition of exchange transactions with the company’s assets.

2.2. Operations

2.2.1. Token Loan Receivable

Under the liquidation model, both tokens transferred and proceeds from sales of such tokens are treated as TI’s assets held in the custody of an MM. When tokens are sold on the exchange, gain/(loss) is recognized by TI using the cost basis of tokens and the fair value of sale proceeds.

The remittance of proceeds from the MM back to the TI is essentially a transfer of cash between two financial institutions. For example, assume the MM received stablecoins in exchange for tokens sold on behalf of the TI. The TI’s chart of accounts should allow separate tracking of stablecoins held with the MM and those held in the TI’s wallet. A transfer of stablecoins from the MM’s account to the TI’s wallet does not result in recognition, derecognition, gains, or losses.

Under the loan/call option model, the token issuer (TI) does not account for sales and purchases of tokens executed by the market maker (MM). Instead, the TI continues to account for the token loan receivables (amounts the MM owes for the borrowed tokens) and the related call option derivative (a financial instrument that gives the MM the right to buy tokens at a set price) until the loan has been repaid.

Under the retainer fee model, the TI does not make accounting entries for token sales and purchases made by the MM. This means TI does not directly record the MM's trading activities related to its tokens.

US GAAP does not explicitly address accounting for the lending of tokens. We summarized below the latest views expressed on this topic within the AICPA’s Practice Aid “Accounting for and Auditing of Digital Assets“ and Deloitte’s Guide “Digital Assets“:

Loaned tokens are derecognized upon transfer, with the corresponding token loan receivable initially measured at the fair value of the tokens at the time of the transfer.

Subsequently, the token loan receivable is remeasured based on changes in the token's fair value.

The current expected credit losses allowance is determined by analogy with the requirements of ASC 326.

Token interest income may be presented as “Interest income” along with fiat interest income.

Under this view, token loans are accounted for similarly to loans denominated in foreign currency, where the issuer’s own tokens serve as such foreign currency. It is important to note that, consistent with ASC 815-15-15-19, it would not be appropriate to analogize the embedded derivative accounting guidance that addresses certain foreign currency derivatives.

2.2.2. Call Option

Typically, the token loan (market-making) terms incorporate a call option as part of a single agreement. As such, a single legal document governs the two instruments (i.e., a token loan receivable and a call option).

However, the call option is NOT a freestanding instrument because it is neither:

Separately entered into, nor

Legally detachable and separately exercisable.

The token loan receivable is not a derivative, as it requires an upfront investment equal to the notional amount. As such, the call option attached to a token loan is accounted for separately from the token loan receivable using the guidance for embedded derivatives.

Below, we assume that hedge accounting does not apply.

2.2.2.1. Identification and bifurcation

The embedded derivative related to the call option should be evaluated under the requirements of FASB ASC 815-15-25-1 to determine whether an embedded derivative requires bifurcation and separate accounting. The following conditions should be met for the embedded derivative to require bifurcation:

A) CLEARLY AND CLOSELY RELATED CRITERION.

Requirement:

The economic characteristics and risks of a call option should not be closely related to the token loan contract.

Analysis:

The host contract of this hybrid instrument is a debt instrument because it has a stated maturity and does not grant voting rights or entitle shareholders to receive distributions. The embedded derivative is a token-based derivative that has as its underlying the fair value of the issuer’s token.

The call option gives the MM the right to settle in stablecoins using the token value based on a contractually fixed price. That option subjects the arrangement to an additional market price risk that is not inherent to the debt instrument. As such, the call option is not clearly and closely related to the host contract and must be separated from the host contract and accounted for as a derivative.

B) SEPARATE INSTRUMENT CRITERION.

Requirement:

If entered separately under the same terms, the call option should fall within the scope of ASC 815.

Analysis:

We need to determine whether the embedded derivative issued as a separate instrument would have characteristics listed in FASB ASC 815-10-15-83(a) – “Underlying, notional amount, payment provision” and 815-10-15-83 (c) – “Net settlement”, and would not fall under any of the ASC 815 scope exceptions.

The characteristic (a) “Underlying” is present as the contract has as its underlying the fair value of the issuer’s token receivable.

The characteristic (a) “Notional amount or payment provision or both” is present because the token loan contract has the notional amount (which is the number of tokens borrowed) and also a payment provision that specifies a fixed or determinable settlement to be made if the fair value of tokens reaches the strike price (i.e. if the underlying behaves in a specified manner).

The characteristic (c) “Net settlement” is present, as the contract provides for the delivery of readily convertible to cash assets, which puts the recipient in a position not substantially different from that of net settlement.

We believe that none of the scope exceptions apply, as the loan is denominated in the issuer’s own tokens, which cannot be analogized to foreign currency or equity instruments.

C) FAIR VALUE OPTION CRITERION.

Requirement:

The token loan receivables should not be measured at the fair value.

Analysis:

Under ASC 825-10-15-4, reporting entities may elect to account for token loan receivables under the fair value option (FVO). This election is being made on an instrument-by-instrument basis and is irrevocable. If the FVO is elected, the embedded derivative is not bifurcated and separately recognized. Furthermore, if the FVO is elected, the entity would also not be required to determine the allowance for currently expected credit losses on token loan receivables by analogy with ASC 326.

It should be emphasized that the fair value option refers to the election to remeasure the fair value of the receivable, not the fair value of the underlying tokens. The fact that the token loan is remeasured based on the fair value of tokens does not indicate that the loan receivable is measured at its fair value.

Finally, option calls with barriers are not as intuitive or easy to value for anyone who is not regularly practicing the valuation of similar assets. Excel might be suitable for calculating the fair value of relatively straightforward call options, but in scenarios where the call option valuation requires the use of a binomial lattice model or Monte Carlo simulations, it might be beneficial to measure the fair value of token loan receivables as a whole to avoid unnecessary complexities.

Conclusion:

If all three criteria above are met, the call option requires bifurcation and should be separately accounted for as an embedded derivative, initially and subsequently measured at fair value.

2.2.2.2. Measurement

The valuation approach might be different depending on the specific terms of a call option:

For a European-style option (both strike price and expiry date fixed at inception) and an American-style option without yield or with a yield rate below the respective risk-free rate, we could use the Black-Scholes-Merton technique, specifically, the closed-form solutions of Reiner & Rubinstein.

For an American-style option (exercise is allowed at any time before expiry) with a yield that exceeds the risk-free rate, a lattice/binomial model would be more appropriate.

For an option with path-dependent settlement (e.g., a future TWAP or a present price barrier), a Monte Carlo valuation technique would be more suitable.

Several free tools are available to measure the fair value of this option, including DerivaGem and QuanLib. However, using these tools without performing appropriate testing and authorization may later result in an internal control deficiency unless you address all relevant process risk points appropriately. It is also possible to calculate this value in spreadsheets (see a link to our illustrative spreadsheet at the end of this section). Bloomberg Terminal is also an option.

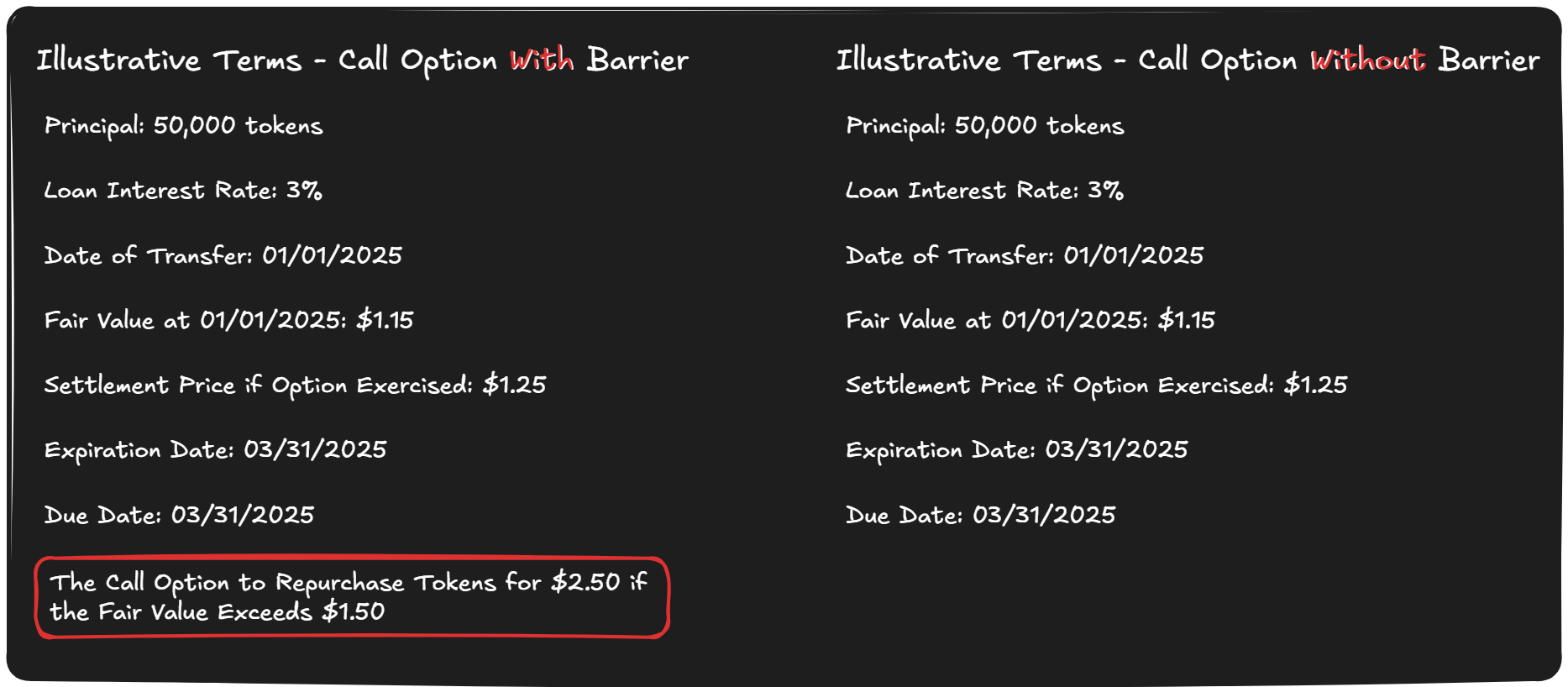

For illustration, let’s analyze a market-making arrangement with the following details:

Let’s also assume that:

The annual token inflation is 8%.

CoinDesk Overnight Rate (CDOR) as of 01/01/2025 is 12.53%

Historically, the token price volatility was 111.44%, and this is not expected to change in the future.

The key inputs used to calculate the fair value of a strike option include:

Barrier Option type: “Up-and-in call”

Up: because the barrier is above the current spot.

In: because the option only knocks in (activates) when the barrier is reached.

Call: because the right is to buy at the contractual price.

Spot price: $1.15 per token [the fair value as of the inception date]

Dividend yield: 8% [the annual inflation rate of the token based on the anticipated reduction in the price]

Interest rate (Risk-free rate): 12.53% [Normally, a risk-free rate is determined based on the yield rates of U.S. Treasury notes for the respective contractual term of an instrument. We suggest a possible alternative approach that utilizes Coindesk Overnight Rates for USDSC on AAVE, available here; however, this approach may be inappropriate in certain scenarios. Without knowledge of specific facts and circumstances, reporting entities have to consult with their advisors prior to using this approach.]

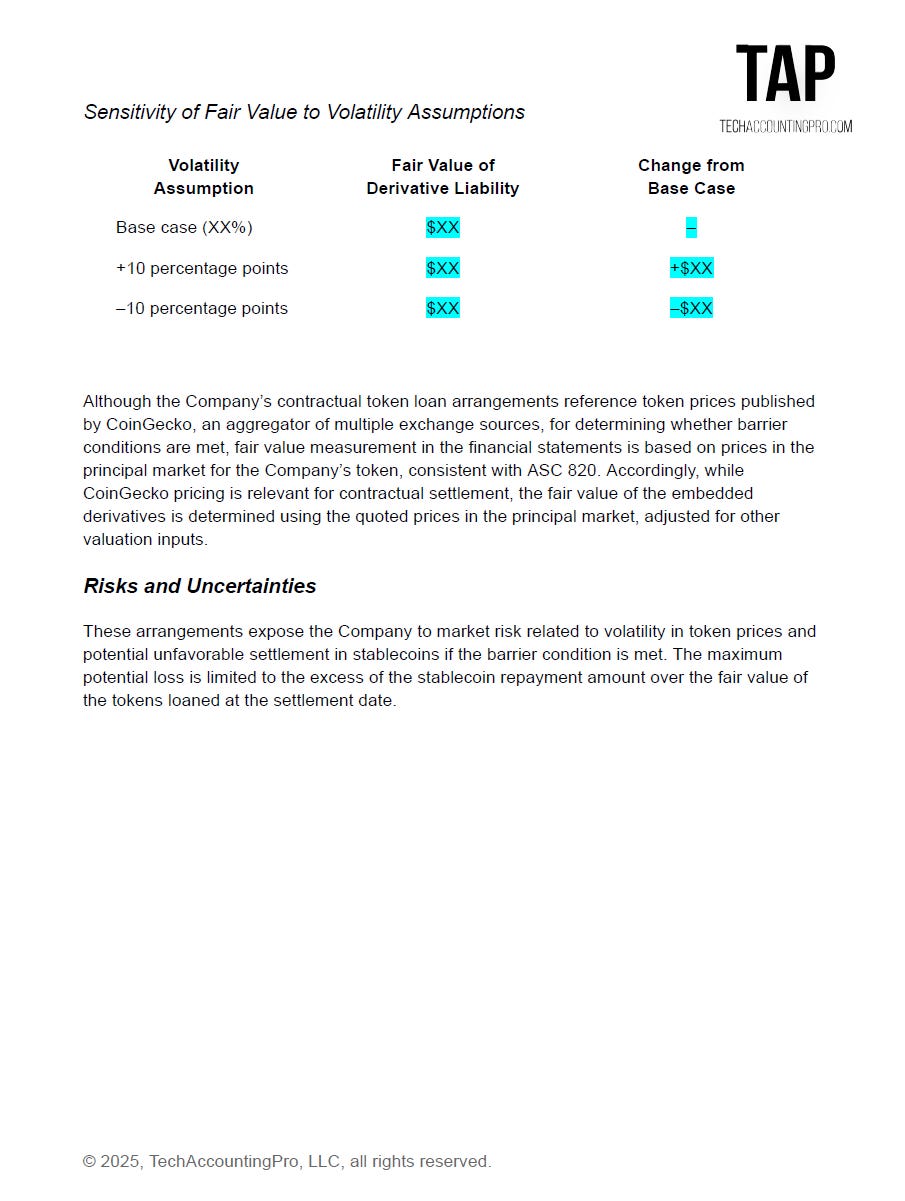

Volatility: 111.44% [Here, the analysis needs to account for the fact that the MM’s own activity is designed to reduce the spread and thus distorts the observed volatility in a way that violates the market participant premise of ASC 820. As such, reporting entities should attempt to use the implied volatility (when an active market exists for token options) or, otherwise, use historical or comparable token volatility. The best practice is to inform users about the effect of changes in the volatility assumption in a sensitivity disclosure within the footnotes to the financial statements.]

Strike: $1.25 [This is stated in the contract price for the purchase of tokens based on the exercised MM call. This price is often calculated as a Token Weighted Average Price (TWAP) over an agreed-upon period.]

Maturity (in years): 0.2056 [As per our example, from the time when tokens were transferred to MM (on 1/1/2025) until the option expires (on 3/15/2025).]

Rebate: $0.00 [In barrier options, a rebate is a cash amount paid upon either failure to achieve the barrier or termination. It’s non-zero only if the contract explicitly promises some payment when the main option doesn’t deliver its usual payoff.]

Additional adjustments: [The payoff is defined at expiry, but settlement is delayed; therefore, we add an extra discount factor to account for the lag between the call option expiry date (03/15/2025) and the loan settlement date (03/31/2025).]

Barrier level: $2.50 for Call Option With a Barrier and None for Call Option Without a Barrier [A barrier is a pre-set price level of the underlying asset that, if reached, either activates (knock-in) or extinguishes (knock-out) an option.]

Refer to the details on how to measure this call option in our illustrative gsheet.

2.2.2.3. Recognition

The following journal entries would be recorded at inception and subsequently at interim periods:

Recognize the token loan receivable:

DEBIT Token loan receivable

DEBIT Unrealized loss

CREDIT Digital assets

CREDIT Unrealized gain

Recognize the embedded derivative liability at fair value:

DEBIT Token loan receivable - Premium

CREDIT Embedded derivative liability

Remeasure the embedded derivative liability at fair value at interim periods:

DEBIT Unrealized loss

DEBIT Embedded derivative liability

CREDIT Unrealized gain

CREDIT Embedded derivative liability

Amortize token loan premium:

DEBIT Other expenses

CREDIT Token loan receivable - Premium

It might also be argued that the embedded derivative liability should be accounted for separately from the loan because the purpose of issuing this call option is to pay for services provided by the market maker. As such, in our opinion, the embedded derivative liability might also be recognized as follows:

Recognize the embedded derivative liability at fair value:

DEBIT Prepaid MM fees

CREDIT Embedded derivative liability

Amortize prepaid MM fees through the contract term:

DEBIT Selling, general, & administrative expenses

CREDIT Prepaid MM fees

2.2.2.4. Derecognition

The call option will ultimately be either exercised or will expire. Either of those events concludes the embedded derivative accounting by derecognizing any remaining balance of an embedded derivative and recording the corresponding adjustment to other income/(expense).

Derecognition as a Result of the Exercise

Generally, the debt-modification and extinguishment guidance of FASB ASC Topic 470-50 does not apply to the option exercise because the call option was part of the agreed-upon terms from the loan origination date, and there was no subsequent change. However, amendments to token loan agreements made after the inception date that add or reset the option would be evaluated under the modification guidance.

Upon exercise, the reporting entity will need to record how it:

Derecognize the derivative liability related to an exercised option:

DEBIT Embedded derivative liability

CREDIT Other income

Account for the return of the loan once a stablecoin payment is received as proceeds from the sale of tokens to non-customers:

DEBIT Stablecoins

CREDIT Other income

Derecognize the cost basis of tokens sold to a non-customer:

DEBIT Other expenses

CREDIT Token loan receivable

Account for the realized gains/losses on the transaction:

DEBIT Unrealized gain / Realized loss

CREDIT Realized gain/Unrealized loss

Derecognition as a Result of the Expiration

Expiration of an option will be accounted for using the following journal entry:

DEBIT Embedded derivative liability

CREDIT Other income

2.2.2.5. Presentation

Offsetting the call option-related derivative against token loan receivables is not appropriate, as only MM (not TI) has the legal right to exercise the option. Hence, the company would record the token loan receivable as an asset and the call option derivative as a liability.

Changes in the call option fair value have no impact on the interest income because the derivative reflects market risk rather than the time value of money.

2.2.2.6. Other Considerations

Because token loan receivables are not financial assets, ASC 860 “Transfers and servicing” would technically not be applicable, which creates a significant opportunity for abusive/creative accounting. It will allow reporting entities to recognize income in situations where they would be precluded from doing so when operating with financial assets. At the same time, we would also be cautious of applying ASC 860 by analogy. In-depth analysis is required based on specific facts and circumstances to ensure the appropriate accounting treatment.

2.2.3. Allowance for Credit Losses

ASC 326 includes two practical expedients that permit consideration of the fair value of the collateral at the reporting date when determining the allowance for credit losses. These practical expedients are available in the following two scenarios:

Collateral dependence [ASC 326-20-35-5] for a financial asset where the borrower is experiencing financial difficulty and (based on the entity’s assessment as of the reporting date) the repayment is expected substantially through the operation or sale of the collateral.

Collateral maintenance [ASC 326-20-35-6] when the borrower is contractually required to continuously adjust the amount of collateral securing the financial asset as a result of changes in the fair value of collateral.

In market-making arrangements, token receivables are expected to be repaid substantially through the operation or sale of tokens. Further, the fair value of tokens changes is automatically reflected in the change of the fair value of the token receivables. If the receivable is measured at fair value through earnings under FASB ASC Topic 825-10, no credit loss allowance is required to be assessed for this instrument. Otherwise, when expected credit losses are estimated under FASB ASC Topic 326 and there is a legally enforceable right to liquid collateral with maintenance/margining provisions, the expected credit loss may be immaterial.

2.3. Liquidity Deprovisioning

Under both models, the repayment of tokens is accounted for by crediting the token loan receivable and debiting the account used for tracking held in the issuer-controlled wallet tokens:

DEBIT Digital Assets

CREDIT Token Loan Receivable

However, when the call option (issued under the loan/call option model) is exercised, the settlement of token loan receivables will typically be performed using stablecoins in the amount calculated using the number of tokens loaned and specified in the contract price (usually, using the Time Weighted Average Price or TWAP at the loan inception). Correspondingly, the repayment made using stablecoins is accounted for by crediting the token loan receivable and debiting the stablecoin account:

DEBIT Stablecoins

CREDIT Token Loan Receivable

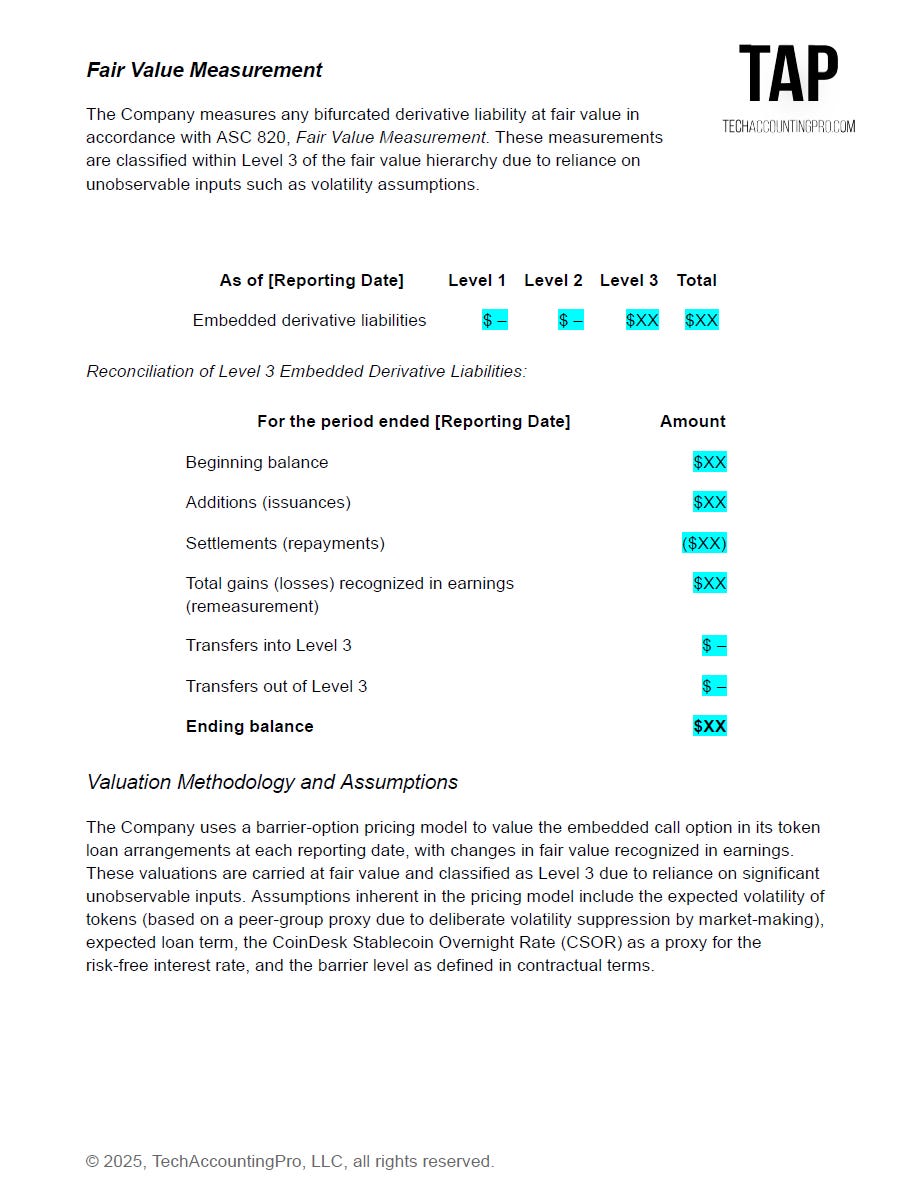

3. Disclosures

Given the complexity and lack of specific guidance for market-making arrangements, reporting entities should include extensive quantitative and qualitative disclosures to enhance the user’s understanding of how market-making affects the entity’s financial position, results of operations, and cash flows. These disclosures should directly address the nature of market-making activities, terms of existing arrangements with market makers, regulatory compliance considerations, accounting policies, and other relevant factors discussed in this article.

Illustrative footnote disclosures are provided here:

Conclusion

Accounting for market-making arrangements in the Web3 and digital asset ecosystem requires advanced expertise in both the crypto landscape and relevant accounting standards. Each model presents distinct accounting and operational considerations.

As the market continues to evolve, it remains essential for reporting entities engaging market makers to monitor regulatory developments and proactively refine their internal processes. To support transparency, mitigate risk, and pursue new opportunities, organizations must conduct thorough reviews and analyses of their arrangements with market makers.

These references outline potential regulatory and market manipulation risks associated with market making in specific jurisdictions. This article does not provide legal advice and cites these points only to identify risk areas management should address with counsel.

However, this ability is limited because the issuer usually relies substantially on the market maker’s expertise, skills, and knowledge.