What Is Acquihiring and How Should It Be Accounted For?

This post discusses the definition and key characteristics of acquihiring transactions, contrasts them with assumptions underlying the corresponding accounting model, and explores further implications

Executive Summary

Acquihiring is a common strategy used by companies seeking access to highly skilled talent, particularly in the tech space. An acquihiring transaction is a transaction in which an acquirer obtains control of a target company primarily to gain access to its workforce rather than its products, customers, or processes. These transactions are most common in technology and other knowledge-intensive industries where highly specialized teams are difficult to recruit organically.

In most acqui-hiring transactions, the acquired entity ceases operations shortly after the acquisition date. Employees are integrated into the acquirer’s organization, and the target’s products and services are discontinued, absorbed, or deprioritized. The principal strategic benefit is the ability to acquire a fully formed, highly specialized team within a compressed timeframe.

Although the transaction value is typically driven primarily by the acquisition of human capital, current guidance frequently results in these transactions being accounted for as business combinations, with workforce-related value subsumed into goodwill and prohibited from separate recognition.

This paper explains the economic characteristics of acqui-hiring, outlines the applicable accounting framework, and highlights structural tensions in how existing guidance captures these transactions. It also discusses common structuring variations, including reverse acqui-hiring, and identifies areas where accounting outcomes may be driven more by technical form than by economic substance.

Economic Substance of an Acqui-hiring Transaction

From an economic perspective, the consideration transferred in an acqui-hiring transaction is paid primarily for the following components:

Contractual workforce-related rights, such as employment agreements, retention arrangements, and non-compete clauses

Non-contractual workforce-related value associated with an assembled team and its collective expertise

Intellectual property, including developed technology, in-process research and development, or internal-use software

Any existing business processes are often incidental to the transaction and are not expected to continue in their pre-acquisition form.

Applicable Accounting Models

Under US GAAP, an acqui-hiring transaction must be accounted for using one of two models:

The acquisition method for business combinations

The cost accumulation model for asset acquisitions

The determination of the applicable model is governed by whether the acquired set meets the definition of a business under ASC 805. The accounting framework does not provide a separate model for transactions primarily motivated by workforce acquisition. As a result, acqui-hiring transactions are forced into one of these two existing models.

Determining Whether an Acqui-hire Is a Business

Under FASB ASC 805, Business Combinations, the buyer should determine whether features of the acquired set indicate that a new business needs to be integrated with the acquirer’s existing business. This determination is based on the two-step process designed to assess whether the FASB’s formal definition of a business in ASC 805-10-55-3A through 805-10-55-9 has been met in the context of a set.

Step 1: Concentration of Fair Value Test.

The first step evaluates whether substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or a group of similar identifiable assets. If this test is met, the acquired set is not a business.

In acqui-hiring transactions, a significant portion of the transaction value is often concentrated in the assembled workforce. However, because an assembled workforce is not an identifiable asset for purposes of ASC 805, it is excluded from the concentration test. As a result, transactions in which workforce-related value clearly dominates the economics may nonetheless fail the concentration test.

Step 2: Business Definition (Inputs and Processes) Test.

If the concentration test is not met, the acquirer must assess whether the acquired set includes both inputs and substantive processes that together have the ability to create outputs.

“A business is an integrated set of activities and assets that is capable of being conducted and managed for the purpose of providing a return in the form of dividends, lower costs, or other economic benefits directly to investors or other owners, members, or participants.”

[FASB ASC 805-10-55-3A]

While a workforce alone does not constitute a substantive process, in practice, the combination of a workforce and intellectual property often leads to the conclusion that a substantive process exists. In acqui-hiring transactions, however, these processes are frequently economically insignificant and are not expected to generate outputs independently post-acquisition.

Accounting Outcomes

Under both models, an acquirer typically recognizes additional assets that are not present on the balance sheet of the target. This is because the transaction provides evidence that internally generated intangible assets of the target do actually exist and has external value supported by empirical evidence.

Accounting standards require accounting to reflect the financial position and changes thereto from the perspective of a general user of financial statements. From the perspective of this general user, the nature of the set acquired, rather than its intended purpose, determines the transaction accounting treatment.

For the same reason, the fair value of individual assets (which is important for both types of transactions) is determined based on market participant assumptions, hence, specific buyer’s intentions regarding the use or abandonement of an asset do not change the fair value measurement, because other market participants might be willing to pay for the asset.

Business Combination Accounting

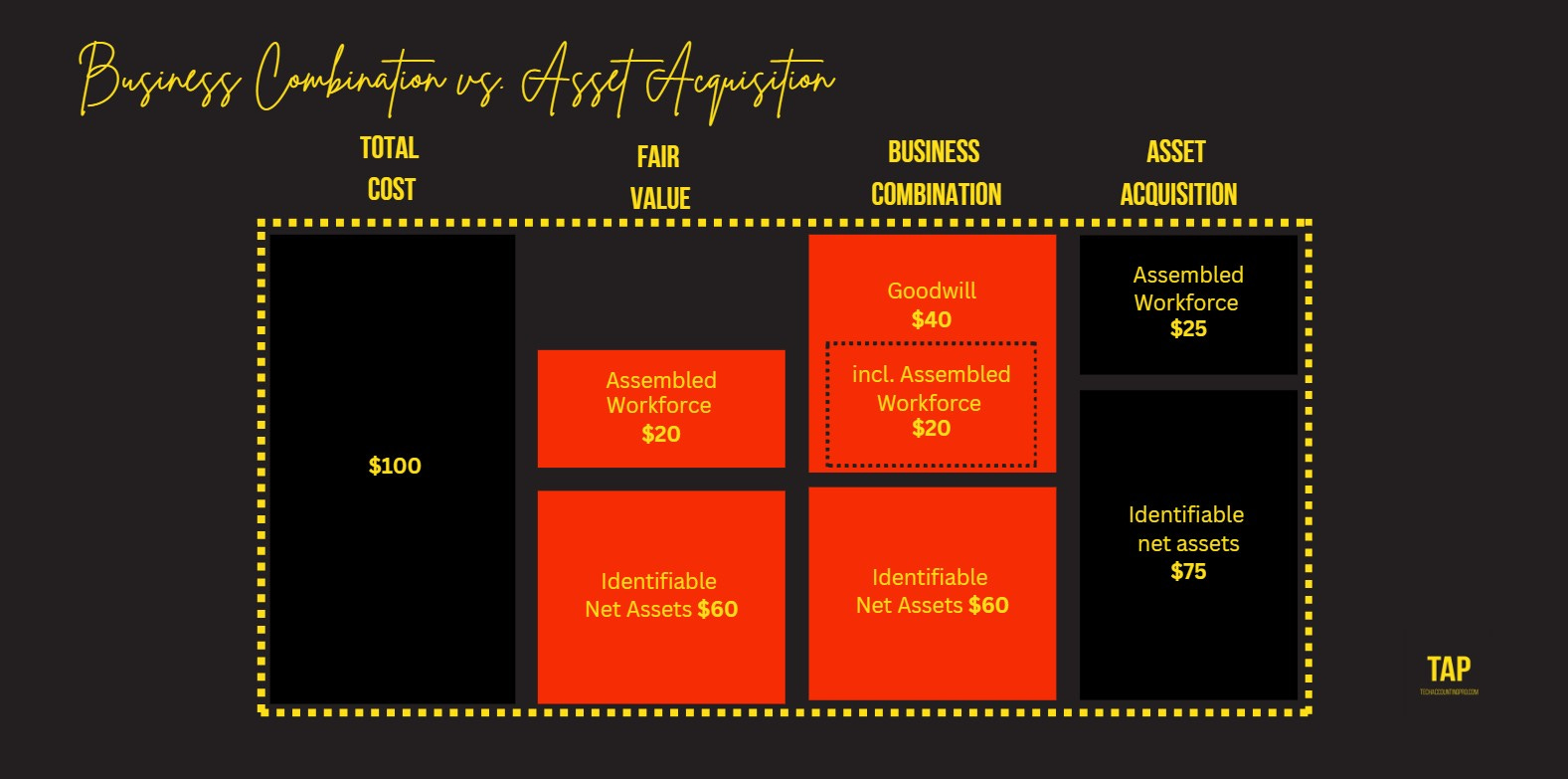

In a business combination, the acquired set is a business, and a business is more than just a sum of its individual parts. Thus, identifiable assets and liabilities are recognized at fair value as of the acquisition date, and any excess of the consideration transferred over the fair value of identifiable net assets is recognized as goodwill.

Goodwill arises because the transaction price is negotiated for a going concern. Economically, goodwill represents the present value of expected abnormal returns that exceed the normal return on identifiable net assets. These returns only exist because the assets are already organized into a functioning business.

Transaction costs are expensed as incurred because capitalization as part of cost of identifiable assets would result in a cost basis different than the fair value of individual assets

Asset Acquisition Accounting

In an asset acquisition, the acquired set is not a business. Therefore, the set is just the sum of individual assets and liabilities acquired, and nothing more than that. Hence, standard cost accumulation model is followed where we assign total cost (including liabilities assumed and transaction costs) of transaction to all assets acquired. based on their relative fair values. No goodwill is recognized.

Assembled Workforce Accounting

Business Combinations

ASC 805 prohibits the separate recognition of an assembled workforce in a business combination [ASC 805-20-55-6]. An assembled workforce does not meet the definition of an identifiable intangible asset because it is not separable and does not arise from contractual or legal rights.

As a result, its value cannot be measured separately from the overall business and is instead included in goodwill.

The accounting framework intentionally treats assembled workforce differently from other intangibles in a business combination. Goodwill represents the residual value of the acquired business after identifiable assets and liabilities are recognized, and the value attributable to an assembled workforce is included in that residual.

Two examples of acquihiring transactions accounted for as business combinations:

Glu Mobile, Inc. acquired Dairy Free Games, Inc., a small mobile game studio, for $2m cash as discussed in the filing available here. The deal was treated as a business combination. Identified intangibles included in-process R&D for the game under development. About $0.6 million was recorded as goodwill attributable primarily to synergies and assembled workforce.

Acquisition of MediaCrossing, Inc. by Kubient that was explicitly identified as the acqui-hire in the buyer’s Form 10-K. Although the legal form was an Asset Purchase Agreement (available here), Kubient concluded that the acquired set constituted a business and a deal was accounted for as a business combination. The goodwill was attributed primarily to business reputation, assembled workforce, and anticipated synergies.

Asset Acquisitions

In an asset acquisition, an assembled workforce may be recognized as an identifiable intangible asset because the transaction price provides observable evidence of value. The assembled workforce is measured by allocating transaction price among assets acquired based on their standalone fair values. The standalone fair value of the assembled workforce is typically determined using a replacement cost method. The allocated cumulative costs assigned to the assembled workforce are amortized over expected useful lives.

An example of acquihiring transaction accounted for as an asset acquisition can be found in Form 10-K of Maximus, Inc. Maximus reports that on February 14, 2024, it acquired part of an IT vendor that had been providing services to the company. Cash consideration was 18.0 million dollars. Maximus states that almost all of the consideration ($17.9m) was allocated directly to the most significant asset, the assembled workforce, which was recognized as an intangible asset and amortized over eight years.

How to Appropriately Account for Employee Payments and Other Transactions Separate from Acquihiring?

Careful evaluation is required to distinguish consideration transferred for the acquired business or assets from payments related to separate transactions, including compensation for post-acquisition services.

Amounts attributable to pre-acquisition services required to consummate the transaction are included in the purchase price.

Amounts attributable to post-acquisition services1, retention arrangements, or continued employment are recognized as compensation expense in the post-acquisition financial statements. We should also note that if the legal documentation of the deal specifies that a portion of contingent consideration paid is linked to the permanence of the seller acting in its capacity as an employee of the combined entity, this portion should be excluded from the transaction price and accounted for as compensation.

In acqui-hiring transactions, interdependencies between transaction consideration and compensation arrangements can complicate this analysis, particularly in reverse acquihiring transactions.

EXAMPLES

Payments treated as a part of the transaction price:

Payments required to consummate the transaction

Replacement awards attributable to pre-transaction service

Earnouts contingent on acquired business performance or nonemployee conditions

Severance payments to terminated employees

Replacement of existing stock awards based on the law or pre-existing obligations

Stock options vested upon a change in control.

Payments treated as compensation expense:

Fees paid under the transition service agreements (in acquihiring such agreements are less common and typically narrower in scope than in traditional acquisitions)

Replacement awards attributable to post-transaction service

Voluntary replacement of existing stock awards that expire upon a change in control

Excess of the fair value of the replacement awards over the fair value of the acquiree’s award for which employees have rendered the required services as of the acquisition date

Earnouts contingent on continued employment or retention metrics

What is Reverse Acquihiring?

In addition, there is also what is generally known as “reverse acquihiring”. In a reverse acqui-hiring structure, the acquirer does not acquire the target entity. Instead, it licenses technology or intellectual property and hires employees directly through individual employment agreements.

The target entity may be dissolved or continue to exist, but with limited ongoing operations. For the acquiree, this transaction is not a liquidity event; however, payments for the licensing of existing technology are intended to provide fair compensation to existing investors (and employees who do not receive an employment offer).

These arrangements are generally accounted for as multiple separate transactions rather than as a business combination. No assembled workforce or goodwill is recognized. Payments for employment are treated as compensation, and licensing arrangements are accounted for under the applicable guidance for intangible assets.

Great examples of reverse acquihiring deals were discussed in the following Substack post:

What Features of Acquihiring are not Reflected in Existing Accounting Models?

Overall, asset acquisition accounting is suited for a deal with no expectation of integrating the new business into the existing business. On the other hand, a business combination is suited to a deal where integration is expected (or at the very least possible). However, the economic features of an acquihiring deal do not always align with this view. In particular:

The mere presence of an assembled workforce is traditionally viewed as an indicator that the acquired set includes a substantive process, hence, meets the definition of a business. Yet, an acquihiring transaction is distinct from other acquisitions specifically because the target’s substantive processes (if any) are typically considered insignificant and even irrelevant to the deal motivation and the transaction price calculation. If the acquired set does not include an economically meaningful component related to such a process, it might be argued that the transaction does not involve a business combination and should instead be treated as an asset acquisition in the general case.

In an acquihiring transaction, the transaction value is often concentrated primarily in an assembled workforce. This effectively provides additional assurance regarding the value of the assembled workforce acquired, similar to that in an asset acquisition (which is the underlying rationale for recognizing assembled workforce intangibles in an asset acquisition but not in a business combination transaction).

The differentiation between accounting for a business combination and an asset acquisition is often driven by where the transaction value is concentrated. However, because ASC 805-20-55-6 does not permit separate recognition of the assembled workforce in a business combination, the screen test does not consider the concentration of value in this asset in determining whether the transaction should be treated as an asset acquisition or a business combination.

However, under the existing guidance, the acquisition strategy increases the likelihood that a transaction will be classified as a business combination and that the value of the assembled workforce will be assigned to goodwill.

Additionally, normally, employee compensation arrangements are accounted for separately from transactions. However, in acquihiring, interdependencies might exist between the transaction price and compensation, which may not be resolvable using traditional accounting methods. This is particularly true for reverse acquihiring, where employment and licensing arrangements are recognized on a per-contract basis.

Conclusion

Although existing guidance provides a reasonably practical framework, its application to acqui-hiring transactions can produce results that emphasize technical form over economic substance.

As acqui-hiring continues to be a common transaction strategy, careful judgment and robust documentation are required to ensure that accounting conclusions appropriately reflect the nature of the acquired set and the drivers of transaction value. If your team is involved in an acqui-hiring transaction, please reach out to share your experience and observations.

Frequently Asked Questions About Acqui Hire Accounting

If the startup has no customers or revenue, can it still be a business?

It depends. An acquired set does not need to have revenue or customers to meet the definition of a business, provided it includes inputs and substantive processes capable of producing outputs, an organized workforce, and an input that it can develop and convert into an output.

Does the presence of employees automatically mean the set is a business?

No. A workforce alone does not constitute a substantive process under ASC 805. While employees are often essential to operations, their mere presence does not demonstrate the existence of an organized process capable of producing outputs. To qualify as a business, there must be evidence of structured activities, workflows, or operating systems that extend beyond individual employee skills.

Can we record an assembled workforce intangible even if the purchase agreement does not mention it?

Yes. In an asset acquisition, recognition is based on the substance of the acquired asset rather than the contractual labels used. If the acquired set includes an assembled workforce and that workforce has measurable value, it may be recognized as an intangible asset, even if it is not explicitly named in the purchase agreement. The existence of an arm’s-length transaction provides evidence of value, and the asset is measured based on relative fair value.

Do the accounting treatment of transaction costs differ between business combinations and asset acquisitions?

Yes. In a business combination, transaction costs are expensed as incurred and are not included in the purchase price. In contrast, in an asset acquisition, transaction costs are capitalized into the cost of the acquired assets.

How do companies account for non-compete clauses acquired in acqui-hiring transactions?

A non-compete agreement is a contractual right that restricts an individual or entity from engaging in specified competitive activities for a defined period and geographic area. When obtained in connection with an acqui-hiring transaction, a non-compete may represent an identifiable intangible asset if it arises from contractual or legal rights.

In acqui-hiring arrangements, non-compete clauses are often included to limit founders' or key employees' ability to compete with the acquirer after the transaction. From an accounting perspective, the presence of a non-compete does not, by itself, determine the accounting treatment; rather, the analysis focuses on whether the agreement represents an identifiable intangible asset and has measurable economic value.

If a non-compete meets the definition of an identifiable intangible asset, it is recognized regardless of whether the transaction is treated as a business combination or an asset acquisition. The difference lies in measurement. In a business combination, the non-compete is measured at fair value as of the acquisition date, with any residual consideration recorded as goodwill. In an asset acquisition, the total consideration is allocated to the acquired assets based on relative fair values, and no goodwill is recognized.

In practice, non-compete clauses in acqui-hiring transactions are often not separately recognized. This is because their economic value is frequently limited or highly subjective, particularly when enforceability is uncertain. Valuation depends heavily on factors such as legal enforceability, geographic and temporal scope, and the likelihood that the restriction would meaningfully prevent competitive behavior.

Recent legal developments further affect this analysis. Although the Federal Trade Commission issued a 2024 rule proposing a broad ban on non-compete agreements, it was subsequently vacated and is not in effect. As a result, enforceability remains governed by state law, many of which significantly restrict or prohibit non-competes for certain categories of workers. These limitations often reduce or eliminate the practical value of non-compete agreements.

Accordingly, while non-compete clauses may meet the technical criteria for recognition as intangible assets, they are frequently concluded to have little or no separately measurable value in acqui-hiring transactions. Where recognized, their valuation requires significant judgment and is highly sensitive to assumptions regarding enforceability, scope, and duration.

It should be noted that in acqui-hiring transactions, transition service agreements are usually limited in scope and duration because the strategic objective is to onboard personnel rather than to operate the target’s business.