Customer Crypto Receipts with Near-Immediate Cash Conversion

This post provides insights on the cash flow statement presentation of proceeds from near-immediate conversion of customer crypto proceeds into cash

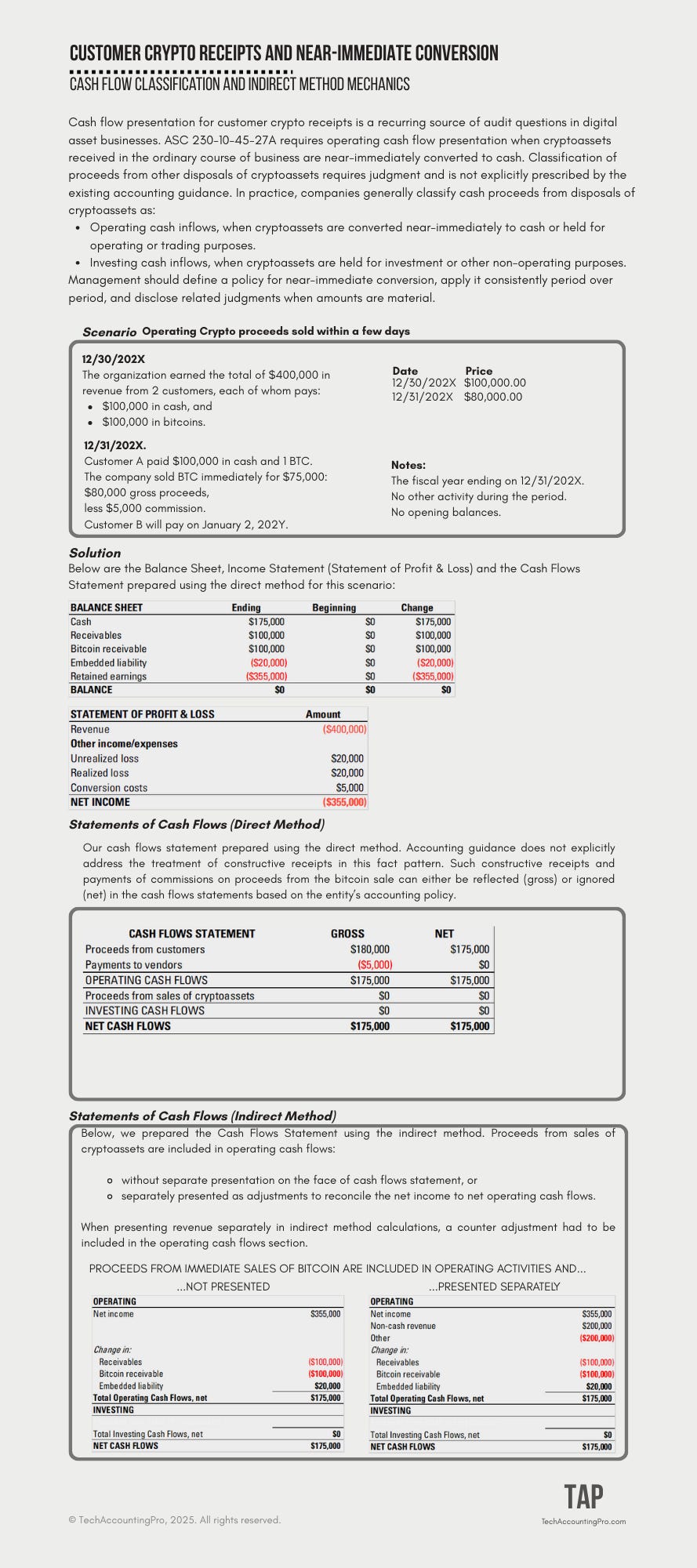

The cash flow presentation for customer crypto receipts remains a recurring audit question in digital asset businesses. ASC 230-10-45-27A requires operating cash flow presentation when cryptoassets received in the ordinary course of business are near-immediately converted to cash. The example below summarizes common classification approaches and the mechanics of the observed indirect methods:

If you think this content might be helpful to someone else you know, please share it.