Daily Low or Daily Close?

This is the question.

I was reading about the SEC comment letter to Cleanspark, Inc. here:

And decided to suggest another point of view about the use of the daily close price instead of the daily lowest price when determining the impairment expense for crypto assets.

Whenever a daily lowest price falls below the current book value of a token, the impairment testing of digital assets is triggered. However, we need to understand that the metric that could serve as a trigger indicator of potential impairment does not by default represent the fair value used to calculate the impairment expense per FASB ASC 350-30-35-19: “The quantitative impairment test for an indefinite-lived intangible asset shall consist of a comparison of the fair value of the asset with its carrying amount. If the carrying amount of an intangible asset exceeds its fair value, an entity shall recognize an impairment loss in an amount equal to that excess. After an impairment loss is recognized, the adjusted carrying amount of the intangible asset shall be its new accounting basis”.

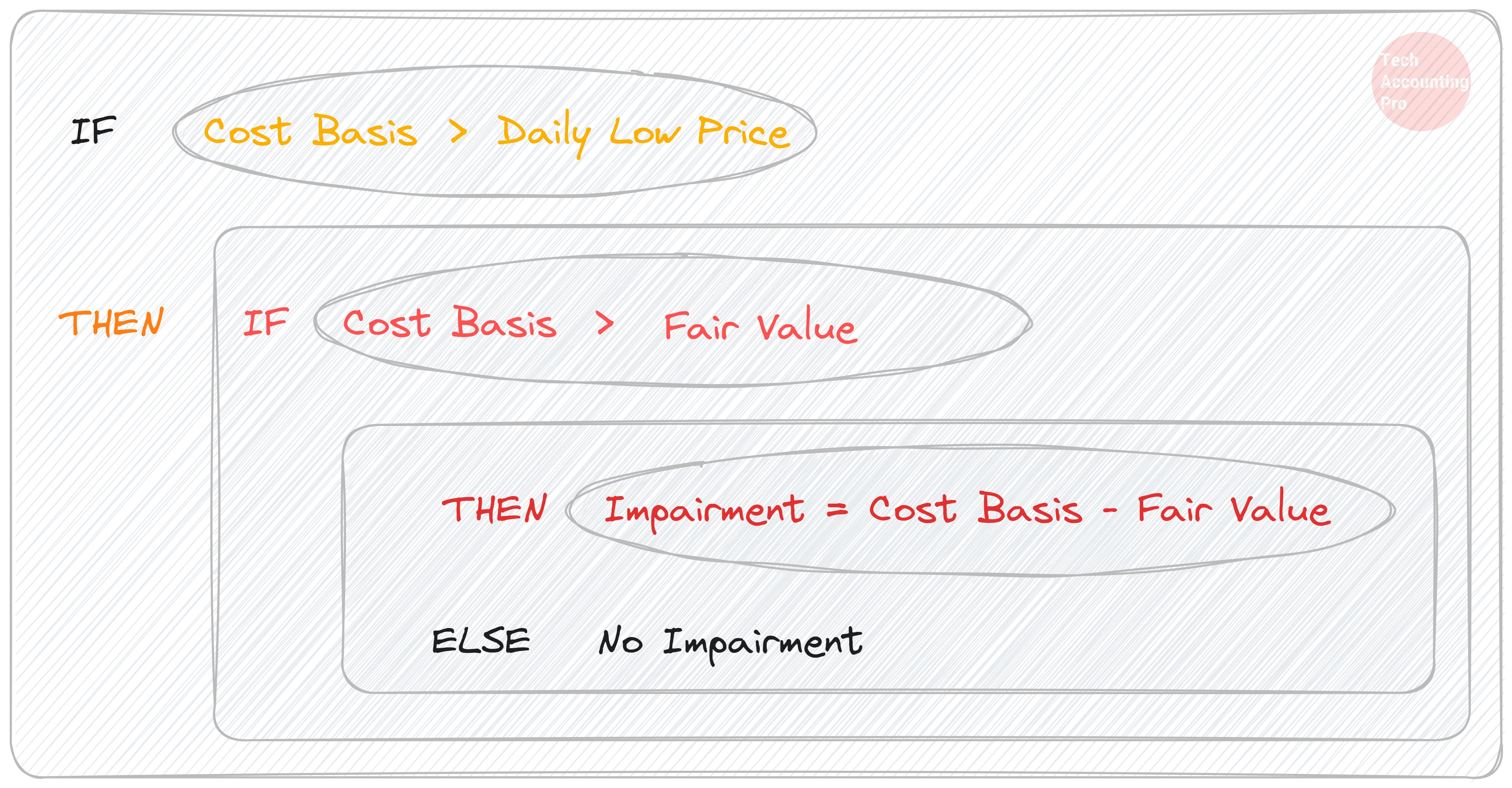

However, the daily lowest price would not constitute the fair value of the asset at the measurement date. Hence, the daily lowest price should not be used in the calculation of the crypto asset impairment charges. Why?

The standard defines fair value as “The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.” [ASC 820-10-20]. Further, as per ASC 820-10-35-9A “Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal (or most advantageous) market at the measurement date under current market conditions (that is, an exit price) regardless of whether that price is directly observable or estimated using another valuation technique.”

We cannot use the daily lowest prices to calculate the impairment charge, as it's unlikely to coincide with the fair value at the measurement date required under ASC 820. Simply put, the standards require measuring the fair value of intangible assets on a full-day basis, regardless of intraday fluctuations. Finally, daily lowest prices (by their nature) often reflect outlier transactions, not representative of an orderly transaction's executable price. The same idea can be found in the answer to the Question 6 in the AICPA’s Guide1.

In a fragmented2 market of crypto assets, determining the principal market's daily low price requires a continuous process. This leads to complicated and ambiguous outcomes that would not be representative of the fair value compliant with FASB ASC 820 requirements.

As such, we believe that the following approach to the crypto asset impairment calculations may be appropriate:

Of course, we are not even touching on the discussion around whether the calculations should be based on bid prices.

American Institute of Certified Public Accountants. (2023). Accounting for and Auditing of Digital Assets, p. 6.

Lukka Prime. (2021). Lukka Prime Methodology Whitepaper.

I suspect we will see more discussion about fair value of crypto assets once ASU 350-60 kicks in.