Defensible Principal Market Pricing for Digital Assets

We explore why current pricing solutions falls short to deliver defensible data about fair values of digital assets and suggest possible solutions

ASU 2023-08 increased pressure on pricing data vendors to provide not only audit-defensible quotes but also robust internal processes to support their data offerings. In other words, the conversation has moved towards fair value governance.

Vendors increasingly market auditable fair-value products rather than simple reference prices. It is obvious that the ability to support a fair value conclusion in a defendable and compliant manner is in demand. Pricing providers have largely built their products around liquid assets traded in observable markets. Illiquid or non-standard holdings create a different evidentiary problem because management may need to support the fair value measurement with unobservable inputs. Valuation of unusual holdings remains an area for exploration. Other common considerations and challenges relate to:

Determining a specific price (ask, bid, or mid),

Clarifying the cut-off timing, and

Providing adequate support.

This post focuses on the following related questions:

How should an entity identify the principal market for a crypto asset?

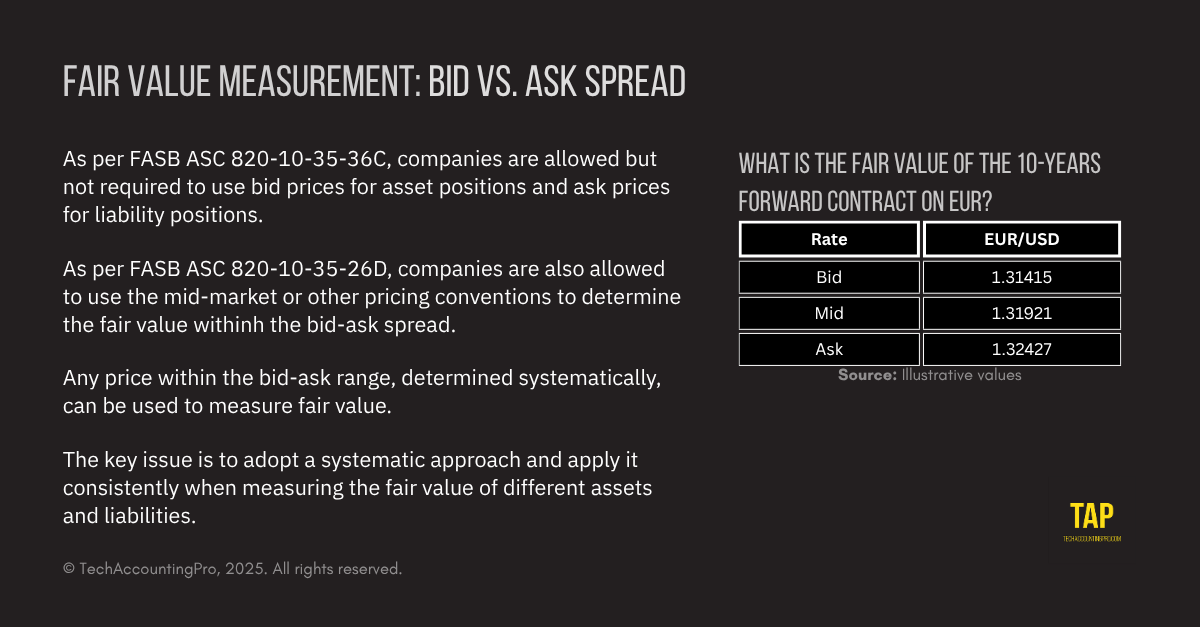

How should management account for the bid-ask spread on a crypto asset?

How should management select the cut-off time for crypto fair value measurements?

How should management assess the reliability of a crypto pricing source?

What evidence should pricing vendors provide to support audit-ready fair value measurements?

When should a pricing vendor be evaluated as a service organization?

Where can reporting teams learn more about crypto asset valuation?

1. How should an entity identify the principal market for a crypto asset?

The principal market is the market with the greatest volume and level of activity for the asset. This should be the market that the reporting entity can access. A market that the entity cannot access cannot be the principal market for that entity’s fair value measurement. Hence, that analysis is entity-specific.

A reporting entity does not need to perform an exhaustive search of all possible markets, but it does need to consider the markets it can access and the information reasonably available to it. In the absence of evidence to the contrary, the market in which the entity normally transacts is presumed to be the principal market.

Tokens, whether well-known or less well-known, are traded on many exchanges with varying liquidity and access restrictions. When an accountant looks up the price of an asset on CoinGecko, they obtain a price aggregated from multiple data sources, not necessarily those to which the reporting entity has access. However, the disaggregated view of prices by exchange/source provided by CoinGecko is a useful resource for initial analysis, provided that the reliability and accuracy of this data are assessed and found to be appropriate prior to using such pricing in the financial reporting process.

In the absence of evidence to the contrary, ASC 820 presumes that the market in which the reporting entity normally would sell the asset is the principal market. The entity does not need to perform an exhaustive search for all markets, but it must consider reasonably available information.

If no principal market exists, the entity uses the most advantageous market. Note that transaction costs may be considered in identifying the most advantageous market, but they are not deducted from the fair value measurement itself. For crypto assets, the practical analysis should focus on access, trading volume, market depth, liquidity, trading restrictions, and the orderliness of observable transactions.

The conclusion should be reassessed when facts change. A change in exchange access, jurisdictional restrictions, liquidity, or market activity may result in a change in the principal market or require additional fair value analysis under ASC 820.

2. How should management account for the bid-ask spread on an asset?

Under ASC 820, the entity should use the price within the bid-ask spread that is most representative of fair value in the circumstances. Selecting the fair value from the bid-ask spread is more nuanced than either blindly accepting the first visible quote or dismissing bid-ask information altogether. A systematic pricing convention, such as midpoint pricing, may be appropriate when applied consistently and reflects market-participant assumptions.

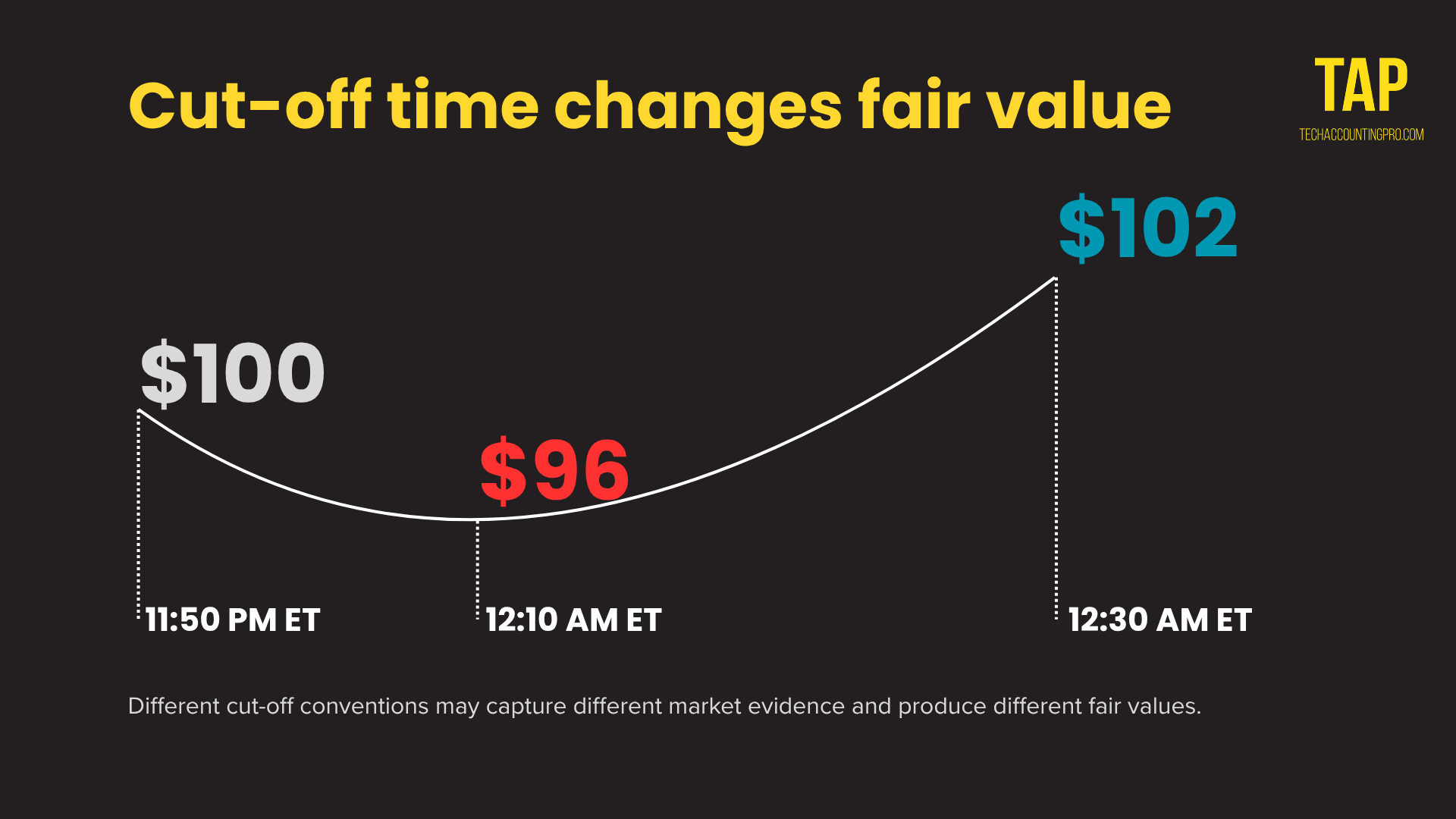

3. How should management select the cut-off time for crypto fair value measurements?

A reporting entity should select a cut-off time that aligns with its reporting process and apply that convention consistently from period to period.

Crypto markets trade continuously, and prices can move materially outside regular business hours. A valuation taken at midnight UTC may differ from a valuation taken at midnight Eastern Time. A valuation taken at the start of an hour may differ from a valuation taken several minutes later.

The selected cut-off should be documented in the entity’s valuation policy. The policy should specify the time zone, time of day, pricing source, and methodology used at that timestamp. It should also describe how management will address market disruption, missing data, delayed feeds, and other exceptions.

Consistency is a key. A reporting entity should avoid changing the cut-off time to achieve a preferred valuation result. Changes to the cut-off convention should be supported by documentation demonstrating that such changes were justified and properly authorized.

4. How should management assess the reliability of a crypto pricing source?

A pricing data vendor is supposed to deliver data to its customers on observable market prices. However, what exactly has been “observed” is not always clear.

There are several ways to assess the reliability of externally sourced information that complement one another and can be used together or separately, depending on the extent and persuasiveness of the evidence already produced. This includes gaining an understanding of the vendor’s processes and methodologies, using this understanding to reconcile with peer and/or source data, and completing independent verification by recomputing results or a sample of pricing data points.

Several vendors now offer fair-value pricing,but end-to-end solutions for harder issues still do not exist for the following gaps:

Visibility into principal-market assessment and how it is tailored to the specific reporting entity, particularly due to:

access to the market (e.g., South Korean exchanges restrict access of foreign investors), or

presumed principal market due to the fact that the entity normally transacts on a specific exchange (even though other markets might have a greater volume or be more advantageous, the reporting entity is not required to perform an exhaustive search across other markets where it does not normally transact).

Incomplete support for custom NAV cut-off times.

No use-case differentiation (fair value of an asset often fluctuates prior to cut-off date; hence, when evaluating the fair value for a specific transaction rather than period-end, it might be more appropriate to use the fair value as of the date and time of such transaction).

Limited transparency around methodology changes or overrides.

Additional analysis is usually required when the portfolio includes restricted assets, thinly traded tokens, NFTs, SAFEs, illiquid coins, or positions that require manually calibrated inputs.

Inconsistent preservation of raw data support, its sources, and exception history in a form that auditors can test.

Management should also evaluate trade completeness when the pricing methodology relies on executed trades. Missing trades can affect last-trade pricing, VWAP, TWAP, and other analysis. For exchanges that use sequential trade IDs, a pricing vendor should be able to identify sequence gaps, attempt to recover missing trades, and document whether unresolved trade IDs were confirmed by the exchange to be non-existent.

5. What evidence should pricing vendors provide to support audit-ready fair value measurements?

A pricing output should be supported by evidence that can be inspected after the reporting date. A reporting entity should be able to explain which pricing source was used, why the source was appropriate, how pricing data points were extracted, what criteria were used to identify exceptions, whether exceptions were identified, and how those exceptions were resolved. It requires a documented, consistent, and thorough process methodology.

For audit purposes, management will often need to support the appropriateness of both the methodology and the data used in the accounting calculation.

Methodology support may include:

The reporting entity’s internal valuation policies;

the vendor’s pricing methodology document, including the applicable version and effective date;

the vendor’s data governance policies; and

An internal memorandum summarizing management’s assessment of whether the vendor’s methodology is consistent with FASB ASC 820 and the reporting entity’s internal policies, including how management addressed any known misalignment.

Data support may include:

System-generated reports or other records showing the relevant pricing data; and

Settings, filters, timestamps, asset identifiers, and other extraction parameters are used to retrieve pricing data from the vendor system.

For trade-based methodologies, support should also address the completeness of the underlying trade population. Management should retain evidence showing either that the trade population was complete or that any missing trade IDs were investigated, resolved, and verified at the exchange level.

Many pricing providers still lack accounting-focused governance processes. Data governance is therefore one of the clearest differentiators in this market. Lukka and Coin Metrics, both well-known platforms in the digital asset pricing market, are notable for their documented approaches, including formalized data governance processes and pricing methodologies.

6. When should a pricing vendor be evaluated as a service organization?

A pricing vendor should be evaluated as a potential service organization when the vendor’s processes and controls, rather than only the data delivered, are relevant to the reporting entity’s financial reporting process.

A pricing vendor generally should not be treated as a service organization when the entity has internal processes to validate and verify pricing data received from the vendor, and those processes operate at a sufficiently precise level.

Management should treat the pricing vendor as a service organization when it relies on the assumption that the vendor follows its stated methodology in practice, or that the vendor’s internal procedures are effective in identifying and resolving outliers and exceptions.

In those circumstances, the entity is relying on vendor controls. Management may therefore need additional procedures to obtain evidence about the operating effectiveness of those controls at the service organization. A SOC report may be useful for this purpose. If the pricing vendor does not have a SOC report, management should implement adequate compensating controls within its own organization.

7. Where can reporting teams learn more about crypto asset valuation?

We note that many users of fair value information might experience issues when first encountering fair value questions. This often results in fund admins and auditors being unable to articulate the specific assumptions and inputs they require to value an asset. This creates a massive opportunity for educational and methodological advisory services. Here are a few resources that we think will be valuable to anyone dealing with this problem:

“Token Design” by Roderick McKinley [here] provides an in-depth understanding of how tokenomics affects the value of cryptoassets.

“Accounting and auditing of digital assets. Practice Guide” by AICPA [here] for non-authoritative answers to common practical questions.

Pricing data vendors that, in our experience, appeared to provide the most useful functionality and in-depth understanding of the accounting standards requirements include:

Key takeaways

The fair value measurement process produces reliable data when it relies on robust governance mechanisms.

Principal market determination and the fair value for crypto assets are entity-specific.

Pricing data aggregators provide information that is insufficient for accounting.

TechAccountingPro can assist with the practical implementation of fair value. Contact us if your team is:

Evaluating a pricing provider’s methodology for compliance with FASB ASC 820.

Drafting internal valuation policies and procedures.

Need assistance in responding to auditor questions.