Liquidity Pool Accounting

The liquidity pools accounting guidance development

A liquidity pool (LP) is a smart contract that holds a pair or collection of digital assets to facilitate decentralized trading, lending, or other financial services without the need for a centralized intermediary. Users contribute assets to the pool and, in return, earn a share of transaction fees or other incentives.

Liquidity pools are core to decentralized finance (DeFi) protocols like Uniswap, enabling continuous, automated exchange of tokens. Each pool operates on pre-set algorithms that determine asset pricing based on the relative quantities of tokens in the pool.

For token issuers, liquidity pools serve multiple strategic purposes, such as:

enabling access to protocol tokens without the need for being listed on a centralized exchange.

acting as a financing and co-marketing tool, particularly when paired with another token project that may lack liquidity. In such arrangements, both projects can benefit from shared exposure and joint participation in the pool, potentially improving market access and community engagement.

While liquidity pools provide income opportunities and flexibility, they also carry risks such as impermanent loss, smart contract vulnerabilities, and price slippage in volatile markets.

Today, we will discuss how liquidity providers should account for assets contributed to the liquidity pools. We will pay particular attention to simulations of scenarios that involve impermanent loss.

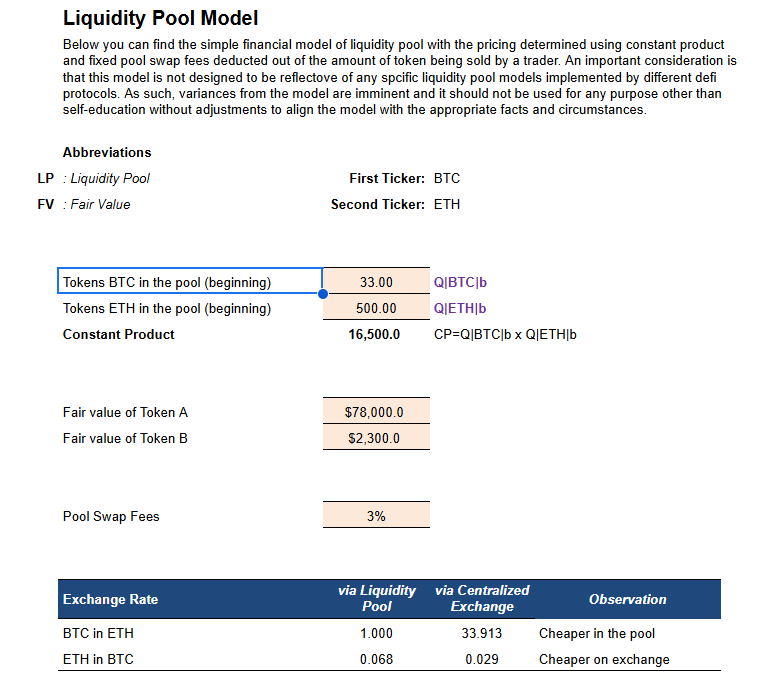

Simple liquidity pool model

We built a simple LP Pool Model spreadsheet.

Our assumptions are as follows:

The liquidity pool contains two tokens.

Each token in the pool is actively traded on a centralized exchange.

Zero costs to purchase or withdraw assets from centralized exchanges.

Deposits to and withdrawals from accounts on centralized exchanges.

Both tokens in the liquidity pool are in the scope of FASB ASC 350-60, hence:

Both tokens in the pool are issued by unaffiliated third parties

Each tokens are accounted for at fair value.

Liquidity pool protocol follows the constant product formula.

The pool charges a fixed rate paid in tokens that are added to the pool.

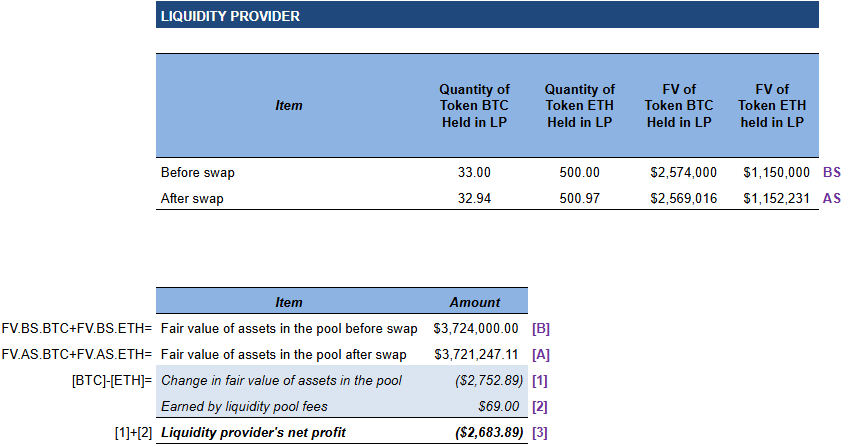

Impermanent Impairment

From this spreadsheet, we can easily see that regardless of what the fair values of each token are and how these fair values change, whenever there is a trade executed by an arbitrage trader who is trying to capture the arbitrage opportunity, the liquidity pool fair value declines exactly in the same amount as the amount of profit earned by the arbitrage trader. This is true regardless of the level of fees set in the pool.

Generally, the effect of executed trades has a different impact on the total value of LP assets depending on the purpose of the trade:

Speculative trades recapture any profit that could have been accumulated from non-speculative trades.

Non-speculative trades might result in profit or loss for the liquidity pool.

The effect of a speculative trade on the trader who executed the trade successfully is calculated in the example used in our model as follows:

On the opposite side, the effect on the liquidity provider is as follows:

However, there is one scenario where the liquidity pool investment will demonstrate an increase in its fair value. This is a scenario where the prices of both tokens are continuously growing (we have often seen these circumstances in real life back in 2020-2021). Here, the fair value of the liquidity pool will increase at a rate consistent with the lowest of the individual price increase rates of each token in the pool.

Accounting Considerations

Liquidity pools are an important component of the blockchain infrastructure. At the same time, there are many factors complicating the LP accounting:

Both the number and price of tokens in the pool are very volatile.

No direct authoritative guidance exists.

Data is rarely readily available for accounting purposes (especially on non-EVM blockchains).

When used as a co-marketing tool or a way to provide financing to other protocols, assets transferred to the pool might be viewed by management as an expense rather than an investment.

The provider’s portion in the liquidity pool is represented in LP shares, which may or may not be actively traded and may or may not accrue liquidity mining rewards.

Logics and the exact mechanism of the asset flows vary significantly because each decentralized exchange (DEX) implementation of liquidity pools is different.

The liquidity pool accounting is the topic that needs a broader discussion and involvement from industry professionals. This is why it is a suggested topic agenda for the future work of the Web3 Accounting Alliance (W3AA). If you’d like to contribute to the discussion and development of the industry-leading guidance around the accounting for liquidity pools, apply to be a contributor in this topic at the next W3AA meeting to be held on 8/21/2025 at 11 AM EST.

Sharp analysis of LP accounting challenges - especially around volatility, data availability, and management intent. Those same themes appear in traditional working‑capital management, where customer payment behaviour, credit terms, and collection efficiency create hidden liquidity risk. TCLM focuses on building transparent, operational financial practices to navigate that complexity. Worth a look if you’re into the intersection of finance and operations.

(It’s free)- https://tradecredit.substack.com/