Stablecoin Classification Under US GAAP and FASB’s New Project on Cash Equivalents

How the FASB’s new agenda could affect the determination of when stablecoins qualify as cash equivalents.

Background

US regulators have begun paying closer attention to dollar-backed stablecoins and their role in financial reporting. On April 4, 2025, the SEC issued a staff statement on “covered stablecoins”. The statement defined “covered stablecoins” as crypto assets designed to maintain a stable value relative to the US dollar, backed by low-risk and readily liquid reserves, and redeemable 1:1 for cash. Although this statement addresses securities law rather than accounting classification, the characteristics it highlights align closely with the existing US GAAP definition of cash equivalents.

Later that year, on October 29, 2025, the FASB added a narrow project to its technical agenda to determine whether certain digital assets, including stablecoins, can be classified as cash equivalents.

Our review of current practice, risk factors, and individual stablecoin designs has led us to three central conclusions:

First, only a narrow group of fiat-backed stablecoins can reasonably meet the criteria for cash equivalents. These tokens must hold high-quality liquid reserves, offer clear and enforceable redemption rights, maintain sufficient market depth relative to the holder’s position, and exhibit a price history largely free from meaningful depeg events.

Second, even when these conditions are satisfied, the classification remains an accounting policy choice. Management should evaluate each specific instrument separately, document the basis for its judgment, and revisit that conclusion if the facts change. Management should maintain clear documentation that supports the selected classification. Best practices include using standard checklists to ensure all necessary facts and circumstances are considered.

Third, many stablecoins do not qualify. Tokens supported by opaque or risky reserves, decentralized or crypto-collateralized designs, or algorithmic mechanisms exhibit risk and liquidity profiles inconsistent with cash-equivalent treatment. Recent court orders freezing hundreds of millions of dollars connected to TrueUSD-related reserves show how governance or legal issues can quickly impair convertibility.

Given these factors, only a small group of well-regulated, fiat-backed stablecoins, such as USDC, and a limited set of peers are likely to be treated as cash equivalents in the near term. Even then, classification should be supported by position size limits, active monitoring of reserve composition and legal structure, and transparent disclosure. For example, a practical guideline for entities could be to set their position size limits to no more than 5% of the stablecoin’s average daily trading volume over the past 30 days. This provides a concrete metric to ensure that a significant liquidation of their position can occur without adversely impacting the market.

What Do Regulators Say About Stablecoins as Cash Equivalents?

On April 4, 2025, the SEC issued a staff statement describing key attributes of “covered stablecoins.” The statement explains:

“Covered Stablecoins are crypto assets designed and marketed for use as a means of making payments, transmitting money, or storing value. They are designed to maintain a stable value relative to USD and are backed by USD and/or other assets that are considered low-risk and readily liquid so as to allow a Covered Stablecoin issuer to honor redemptions on demand.[6]”

[“Statement on Stablecoins”, SEC]

This description prompted market commentators, including Bloomberg and other analysts, to conclude that dollar-backed stablecoins offering one-for-one redemption and immediate convertibility might qualify as cash equivalents under US GAAP. These discussions ultimately contributed to the question being added to the FASB’s technical agenda.

At its October 29, 2025, meeting, the FASB staff presented an overview of current guidance and stakeholder feedback. Views were mixed regarding whether to revise the definition of cash equivalents or develop stablecoin-specific rules. Several stakeholders supported a more principles-based update that would reflect assets without stated maturity, address the treatment of certificates of deposit, and clarify how the definition applies to money market funds.

The emerging direction favored refining the existing definition rather than creating an entirely new category for digital assets. Still, the project remains at an early stage, and the board has not yet indicated the final form of its guidance.

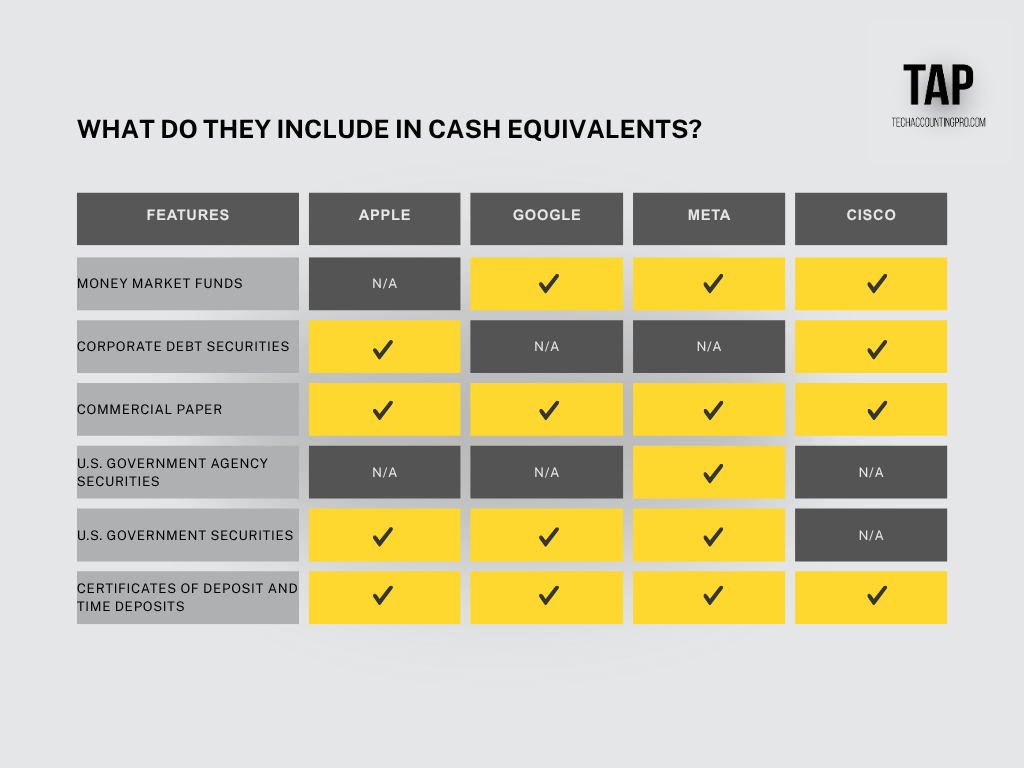

To understand how current practice compares to the formal definition, we conducted a brief review of technology sector Form 10-K filings:

We reviewed a small sample of technology-sector filings to understand which types of instruments public companies include in cash equivalents. The summary below reflects the results.

Across these filings, companies consistently included the same categories of instruments in cash equivalents:

Bank Deposits. Demand deposits and certificates of deposit were consistently treated as cash equivalents. This was true even for deposits with no stated maturity, since the defining characteristic was the immediate availability of funds.

Short-Term Debt Securities. Holdings of U.S. Treasury bills, government agency notes, high-grade commercial paper, and similar short-term instruments (maturing within three months) were included as cash equivalents. For example, Alphabet classified highly liquid government and corporate notes maturing within ninety days as cash equivalents. Cisco included short-term commercial paper, treating these instruments as near-cash due to quick maturity and low risk.

Money Market Funds. Most companies list investments in open-ended money market funds as cash equivalents, often limiting inclusion to AAA-rated funds. Despite lacking a stated maturity, companies relied on their stable value, same-day liquidity, and diversified portfolios to support inclusion as cash equivalents.

Instruments reported within the “Cash and cash equivalents” line on the balance sheet generally share two qualities tied to their short duration:

Minimal credit risk

Insignificant interest rate risk

Instruments that did not meet the maturity, liquidity, or risk criteria were reported elsewhere on the balance sheet. Longer dated marketable securities, for example, appeared within “short-term investments” or “marketable securities” rather than within cash equivalents.

Definition of cash equivalents

Having reviewed industry practice and regulatory guidance, we next examine the formal definition of cash equivalents. Under US GAAP, the definition of cash equivalents is set out in the FASB ASC. Cash equivalents are defined as short-term, highly liquid investments that meet both of the following conditions:

They are readily convertible to known amounts of cash, and

They are so close to maturity that they pose an insignificant risk of changes in value due to interest-rate movements.

In practice, this definition is usually applied using the following benchmarks:

Original maturity of three months or less.

Original maturity is measured from the date the reporting entity acquires the instrument to its contractual maturity date. A three-month Treasury bill qualifies as a cash equivalent. A three-year note purchased with three months remaining also qualifies. A three-year note that has been held for three years does not suddenly become a cash equivalent just because there are only three months left until maturity.Investment nature.

Cash equivalents are investments purchased to earn a small return on surplus cash without exposing that cash to material loss. They are not operating receivables or other non-investment balances.Limited exposure to interest rate risk.

The yield on the instrument can be fixed or variable, but changes in market interest rates during the holding period should not be expected to cause a material change in the amount of cash the entity would receive if it sold or redeemed the instrument before maturity.Active market and known exit value.

The investment should be tradable in an active market or redeemable on demand so that the entity can quickly obtain cash at a reasonably predictable amount. Instruments that are thinly traded, subject to gates, or exposed to significant discounts under stressed conditions generally do not qualify.

It is important to distinguish between:

Any change in fair value, and

Changes in value that arise from interest rate movements.

The FASB ASC Glossary focuses on the latter. An instrument can still qualify as a cash equivalent even if its carrying amount changes over time, for example, as a discount accretes, as long as the only reasonably expected source of variability is that mechanical unwind and any additional variability is clearly immaterial.

Economic purpose also matters. Cash equivalents are typically used to invest idle cash in very low-risk instruments that can be converted into cash on demand for a predictable amount (as per the basis for conclusion in FASB Statement 95). They sit at the very short-duration, very high-liquidity end of the investment spectrum. That is why they are grouped together with cash on the balance sheet and used directly in liquidity analyses that compare “cash and cash equivalents” to current and near-term obligations.

What risks affect the value of cash equivalents?

When evaluating whether an instrument qualifies as a cash equivalent, the relevant question is not “is this an investment” but “what risks can materially affect its value or convertibility.” The main risk categories are:

Interest rate risk.

The impact of changes in market interest rates on the security's value.Liquidity risk, which has two components:

Market liquidity risk refers to the risk of forced sales at prices below observable levels when markets are thin or volatile, for example, during large redemptions or portfolio rebalancing.

Funding liquidity risk is the risk that there is not enough liquidity to redeem the instrument in the required size or timeframe.

Credit risk, which also has two components:

Default risk is the probability that an issuer will fail to meet payment obligations in full and on time. Higher default risk generally leads to greater price volatility and lower liquidity.

Downgrade risk is the risk that the issuer or the instrument is downgraded by rating agencies, which can trigger forced sales at depressed prices.

These risks drive the classification question. If any of them could reasonably result in a material loss of value or a material delay in obtaining cash, the instrument usually does not belong in cash equivalents.

What risk mitigation strategies exist to maintain the stable value?

Traditional cash equivalent portfolios try to maintain stable value through a combination of structural and risk management techniques:

Duration management. Interest rate risk can typically be addressed by limiting the portfolio's weighted-average maturity or duration. Shorter maturities reduce sensitivity to rate changes.

Credit quality monitoring. Default and downgrade risks are managed through the internal credit rating process and due diligence.

Diversification. Most of the risks we identified can be mitigated via diversification. Avoiding excessive concentration in any single issuer, sector, or instrument type.

Short tenor and maturity laddering. Short average maturities and staggered maturity dates help ensure that cash is available ahead of liability due dates.

For most fiat-backed stablecoins, token-level interest rate risk is not directly relevant, as the tokens are usually redeemable on demand at par in fiat currency. However, the reserves backing those tokens carry interest rate and credit risk, and poor reserve management can manifest as liquidity or credit events that threaten the stablecoin’s ability to maintain its peg.

Applying these concepts to stablecoins

Maturity considerations

Maturity is usually measured from the instrument's acquisition date to its contractual redemption date, or to the expected redemption date if early redemption features are substantive.

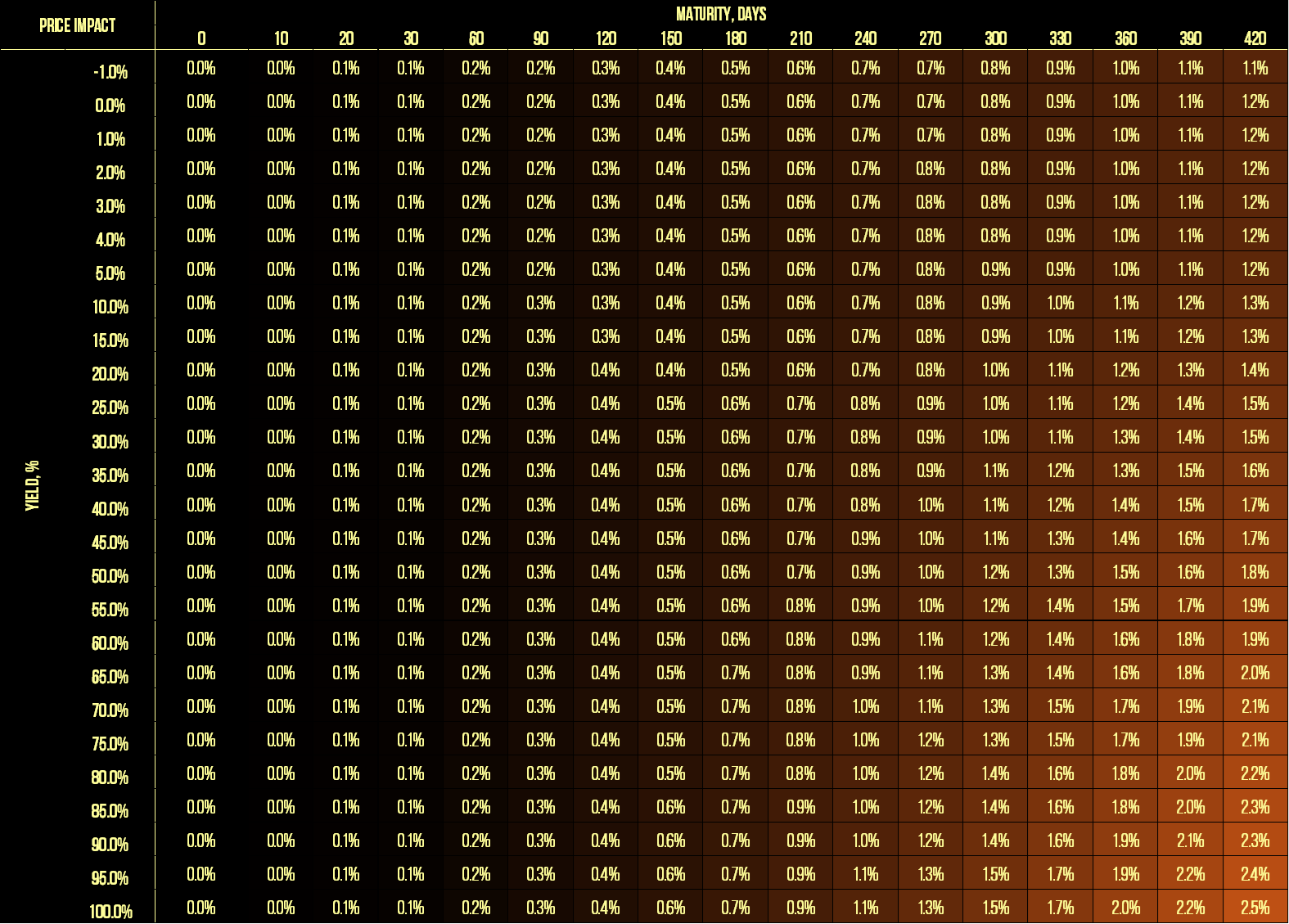

For ordinary debt instruments, longer maturity generally means higher yield and greater sensitivity to interest rate shocks. That logic underpins the conventional “three-month” threshold used in practice: shorter maturity is a proxy for insignificant interest rate risk. The three-month mark also aligns with quarterly reporting cycles, which probably explains its adoption rather than any deep economic principle.

From an economic standpoint, it is more helpful to focus on how much the instrument’s value can move in response to reasonably possible interest rate changes and whether that potential movement is clearly immaterial.

For example, a simple duration-based analysis shows that a one percentage point change in interest rates typically causes less than a 0.5 percent price move for securities with maturities of roughly 150 days or less.

Below is a table that shows the impact of a 1% increase in the market interest rate on the value of instruments with different maturities and original yields. We calculate the price impact as follows:

Percent price change ≈ Duration / (1 + Yield to Maturity) × Δ Yield to Maturity

Under a 90-day threshold, the range is often near 0.2-0.3 percent, suggesting that the exact cutoff is somewhat arbitrary.

Stablecoins behave differently. Most fiat-backed stablecoins have no stated maturity and are redeemable on demand. In effect, the “maturity profile” of a stablecoin aligns with the holder’s own liquidity needs, since the token can be converted to fiat in a time frame that is usually measured in days. As a result, accounting maturity is generally not a helpful factor for stablecoin classification, and interest rate risk is also not relevant.

The key questions we need to ask include:

How quickly can the holder convert the token into fiat under normal conditions?

Under what circumstances can redemption be delayed or denied?

Is there a substantial risk that reserves might not be sufficient to honor redemptions?

Liquidity Considerations

Guidance and practice agree that cash equivalents must be “readily convertible” to cash. As PwC notes:

“The term ‘readily convertible’ implies that an investment must be convertible into cash without an undue period of notice and without incurring a significant penalty on withdrawal… Cancellation clauses, termination fees or usage restrictions might affect the redemption amount and create a more than insignificant risk of change in value.Where the counterparty to a short-term investment experiences financial problems, there may be some doubt over its ability to fulfil the agreement’s requirements. In these instances, the investment should not be classified as a cash equivalent, because there is a risk that the instrument will not be readily convertible or that the redemption obligation will not be met.”

[PwC]

In practice, many analyses of cash equivalents focus heavily on maturity and credit quality, treating liquidity as almost an assumption. For stablecoins, that shortcut is dangerous. Entities must explicitly evaluate both:

Depth and resilience of secondary market trading, and

Practical ability to redeem through the issuer or authorized intermediaries.

A stablecoin might trade at or near one dollar most of the time, yet still be unsuitable as a cash equivalent if the market cannot absorb the entity’s position without significant slippage.

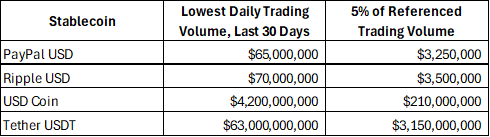

As a suggested guideline, we recommend that entities set internal exposure limits for instruments classified within “cash equivalents.” In particular, a stablecoin should generally not be included in cash equivalents if the reporting entity’s position exceeds a modest share of the token’s typical trading volume. We would suggest avoiding classifying stablecoin holdings as cash equivalents if the entity holds more than 5 percent of the lowest daily trading volume observed over the past 30 days. This type of limit needs to be tailored to the markets and venues the entity actually uses. Regular monitoring will help capture any significant changes in market conditions and ensure that position limits remain appropriate.

The recent experience of our selected stablecoins illustrates this:

For example, a liquidation of approximately $3.25 million of PYUSD might, at certain points in the last 30 days, have represented more than 5 percent of daily trading volume (as per CoinGecko1). In that scenario, classifying the entire position as cash equivalents could overstate the cash that could be realized quickly without a meaningful price impact.

Credit Rating Considerations

For traditional debut securities, credit ratings and expected rating changes may affect liquidity. The lower the credit rating, the lower the liquidity available for the instrument. A change in a credit rating might trigger the forced closure of positions held in this asset.

Stablecoin issuers do not have ratings assigned by credit rating agencies. Instead, S&P initiated “stablecoin stability assessment ratings” published since 2024. Below are some notable ratings:

USDC - 2 Strong (published 12/19/24)

USDT - 4 Constrained (published 12/3/24)

TrueUSD - 5 Week (published 11/14/25)

S&P methodology rates stablecoins based on the following areas of assessment:

Asset assessment

Governance

Legal and regulatory framework

Redeemability and liquidity

Technology and third-party dependencies

Track record

We wanted to note one additional point about the effect of third-party guarantees, such as Coinbase’s promise to all retail users to redeem USDC at a 1:1 ratio. We believe that the value of USDC relies heavily on Coinbase’s adherence to this promise. A change in Coinbase’s credit rating or its potential decision to no longer guarantee USDC redemptions at a 1:1 ratio might significantly affect USDC’s peg stability.

Other Considerations

US GAAP does not explicitly require conversion costs to be insignificant for an investment to qualify as a cash equivalent. However, the line item “cash and cash equivalents” is commonly used in liquidity analysis by comparing it directly with liabilities of various maturities. If significant fees or operational frictions apply when converting a stablecoin to fiat, the amount of value truly available to meet short-term obligations may be meaningfully lower than the reported balance.

For that reason, it is reasonable to consider:

typical and worst-case conversion fees,

slippage from exiting the position in realistic market sizes, and

any operational or regulatory delays in accessing fiat.

Even though these factors are not a part of the existing definition of cash equivalents in accounting authoritative guidance, they are consistent with the economic purpose of the cash equivalents category.

Overall, cash equivalents should be considered a subset of investments with the shortest effective maturities and the highest reliable liquidity. They should be redeemable for cash almost immediately, and until redemption, there should be an active market or a robust redemption channel that allows the instrument to be converted to a known amount of cash with minimal uncertainty.

What is the appropriate accounting treatment of specific stablecoins?

Stablecoins are typically issued by special-purpose entities that hold financial assets as collateral and owe token holders a fixed claim in a reference asset, often US dollars, at a specified one-for-one redemption ratio. In most designs, only institutional customers or certain intermediaries can redeem directly with the issuer, while retail users and many corporate holders rely on trading in the secondary market or on third-party guarantors, where they exist.

From an accounting standpoint, a stablecoin is more likely to qualify as a cash equivalent when:

Reserves are held in cash and very high-quality liquid assets,

Those reserves are legally separated for the benefit of token holders,

The issuer has a consistent track record of honoring redemptions, and

The token trades with tight spreads and limited depeg episodes in stressed markets.

In those cases, the stablecoin can be viewed as economically similar to a money market fund share or a very short-term deposit and may be treated as a cash equivalent, subject to the entity’s accounting policy.

Under current guidance, reporting entities can already elect to include qualifying stablecoins in cash equivalents if the tokens satisfy the authoritative definition criteria. Since designs differ significantly across issuers, management must evaluate each stablecoin individually.

To ensure consistency in this evaluation and appropriateness of conclusions, management should address several points:

1. Collateral Quality: Assess the specific assets backing the stablecoin, ensuring they are not exposed to a significant risk of decline in value. Assess whether the issuer can pledge or lend these assets.

2. Redemption Rights: Evaluate whether holders have an enforceable right to redeem tokens at par, including redemption venues, restrictions, and third-party guarantees present.

3. Market Liquidity: Evaluate the level and stability of trading volumes of the stablecoin analyzed.

4. Price Stability: Examine the frequency, magnitude, and duration of past depeg events, including the issuer’s actions in response to prior stress events, and whether the mechanisms worked as intended.

These steps provide a practical framework for evaluating whether a stablecoin meets cash-equivalent characteristics, enabling consistent, informed decision-making.

In our analysis, fiat-backed stablecoins such as USDC score relatively well on these dimensions. They maintain reserves in short-term Treasuries and cash, publish regular attestations, and offer one-for-one redemption to eligible customers. As a result, they tend to align closely with the economic characteristics of cash equivalents:

As an experiment, we have also built a rating that characterizes the consistency of stablecoins with the characteristics of cash equivalents, which unsurprisingly placed USDC as the most consistent stablecoin in this regard.

By contrast, other categories of stablecoins fall short.

Some fiat-linked tokens have opaque or questionable reserves, weak transparency, or unresolved legal questions.

Decentralized or crypto collateralized stablecoins, such as DAI, involve exposure to crypto asset volatility and usually do not offer a direct claim on fiat reserves.

Algorithmic stablecoins rely on incentive mechanisms and related tokens instead of hard collateral and have historically been prone to collapse.

Algorithmic stablecoins use novel mechanisms (or other assets, such as commodities) to stabilize their value. These include purely algorithmic stablecoins (which have no hard collateral, relying on smart contract algorithms and often another token to absorb volatility) and crypto/commodity-backed tokens (e.g., stablecoins pegged to gold or baskets of assets). Such instruments are far too volatile or insufficiently liquid to be cash equivalents.

A notorious example was TerraUSD (UST), an algorithmic stablecoin that maintained its peg via arbitrage with a sister cryptocurrency and no fiat reserves. It collapsed in 2022, breaking its $1 peg and wiping out billions, illustrating the extreme risk of non-collateralized “stable” assets. Even if an algorithmic stablecoin temporarily maintains a peg, it lacks the guarantee of convertibility into fiat, as there is no pool of safe assets to back its value. These stablecoins should typically be treated as intangible assets and certainly would not qualify as cash equivalents under US GAAP.

Conclusion

In summary, only a narrow subset of stablecoins (those that function essentially like digital dollars) is appropriate to classify as cash equivalents. These stablecoins possess attributes that align with the definition of cash equivalents: they are highly liquid and carry an insignificant risk of value change, making them economically equivalent to holding cash.

On the other hand, many stablecoins should not be considered cash equivalents. Instruments like TrueUSD (TUSD2), despite their dollar peg, lack the full confidence in reserves and enforceable redemption. Decentralized or crypto-collateralized stablecoins like DAI involve inherent market risk and do not provide rights to fiat redemptions. And clearly, any algorithmic or non-fully backed stablecoin falls outside the bounds of a “safe” liquid investment.

As the FASB and regulators continue to refine crypto accounting rules, companies will need to evaluate each stablecoin on a case-by-case basis. The token’s design, collateral quality, legal structure, and the issuer’s governance practices will determine whether a specific stablecoin is reported as “cash equivalents” or falls into other asset categories.

FAQ

Are all stablecoins cash equivalents?

No. Classification as a cash equivalent is not automatic for any stablecoin. It depends on an entity’s accounting policy and whether a particular token meets the US GAAP definition of cash equivalents. Some fiat-backed stablecoins may qualify, but only if management explicitly elects that treatment and can support it on the basis of facts and circumstances.

Should USDC be cash equivalents?

It depends on management’s judgment and accounting policy. We believe there is a strong basis for an entity to elect to classify USDC as a cash equivalent, provided it confirms that USDC’s reserves, redemption mechanics, and liquidity remain consistent with the characteristics of cash equivalents and that the entity’s position size is appropriate relative to market depth.

What is the appropriate treatment of stablecoins under US GAAP?

There is no single standard treatment for all stablecoins. A reporting entity can adopt a policy to treat certain qualifying stablecoins as cash equivalents. Other stablecoins may be more appropriately classified as financial assets measured at fair value, as intangible assets, or under other categories, depending on their rights and risks. Classification should be revisited as market conditions, legal structures, and regulatory guidance evolve.

Data sources such as Coingecko can be useful inputs, but they should not be used in production decision-making without appropriate controls, reconciliations, and monitoring.