Updates to the Measurement of Credit Losses for Accounts Receivable and Contract Assets (FASB ASU 2025-05)

On July 30, 2025, FASB issued ASU 2025-05, 'Measurement of Credit Losses for Accounts Receivable and Contract Assets' that simplify allowances for credit losses on receivables of private entities

On July 30, 2025, FASB issued Accounting Standards Update 2025-05, 'Measurement of Credit Losses for Accounts Receivable and Contract Assets' (the ASU). This update simplifies how companies should provide reserves under the CECL (current expected credit losses) model to current1 customer balances (i.e., accounts receivable and contract assets arising from transactions in the scope of Topic 606, including balances recognized as a result of a business combination).

The following reliefs were provided to entities on a prospective basis for annual periods beginning after December 15, 2025, or earlier for periods for which the financial statements have not yet been issued as of the date when the entity adopts ASI 2025-05:

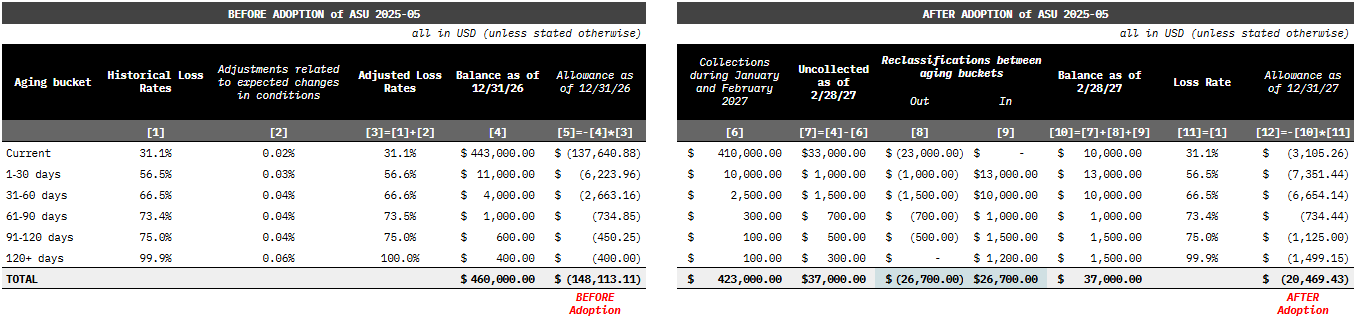

326-20-30-10C introduced a practical expedient that allows us to assume that current conditions as of the balance sheet date will remain through the life of the current customer balances.

326-20-30-10E introduced a policy choice that allows preparers for non-public entities to consider collection activities after the balance sheet date and no later than the date when the financial statements were made available to be issued.

The accounting policy choice under 326-20-30-10E is only granted when a practical expedient under 326-20-30-10C has been elected.

Entities elected to apply the practical expedient/accounting policy choice described above will be required to disclose the elections in the footnotes to the financial statements.

If both the practical expedient and policy choice were elected, then:

No credit loss allowances should be recorded on the amounts collected after the period end and no later than any date selected before the date when the financial statements have been made available to be issued.

Credit loss allowances on the remaining uncollected balances should be recognized based on the delinquency status as of the date when the financial statements have been made available to be issued.

We share the file with sample calculations here:

The term “current” here means that accounts receivable and contract assets are expected to be realized within the one-year period (or longer if the business’s operating cycle exceeds one year).